- LOGIN

- MemberShip

- 2026-05-02 10:13:37

- Company

- ‘Access to bispecific antibody Columvi should be improved’

- by Son, Hyung Min Nov 14, 2024 05:51am

- Dr. Chris Fox, Professor of Haematology at the University of Nottingham, U.K. “Diffuse large B-cell lymphoma (DLBCL) is a disease in which one in four patients experience relapse even after treatment. The bispecific antibody Columvi has demonstrated efficacy in relapsed patients at up to 18 months of follow-up. The clinical performance of Columvi is not just an incremental improvement over existing therapies, but a paradigm shift in the DLBCL treatment environment.” At a recent meeting with Dailypharm, Dr. Chris Fox, Professor of Haematology at the University of Nottingham, U.K., recently described so about Columbo, a bispecific antibody approved for diffuse large B-cell lymphoma in Korea. DLBCL is a disease in which the body's protective “B cells” grow or multiply uncontrollably and is the most common form of non-Hodgkin's lymphoma that accounts for about 40% of all non-Hodgkin's lymphomas. The disease is characterized by aggressive, rapidly progressive staging. The number of DLBCL patients in Korea was 14,183 as of last year, a 36% increase from the 10,428 in 2018. Up to 15% of DLBCL patients fail first-line standard therapy, and 25% of patients experience relapse within 18 months despite achieving a complete response (CR). Patients with relapsed or refractory DLBCL show a characteristically rapidly worsening prognosis as the number of treatment cycles increases. Columvi, the first bispecific antibody targeting CD20XCD3 enters the market...offers the advantage of a fixed dosing period The good news is that a variety of new drugs have emerged for this disease. Roche's Polivy, a representative DLBCL drug, is said to be effective in about two-thirds of patients when used as a first-line treatment. However, this means that about one-third of patients who do not respond to first-line treatment remain in need of further options. Bispecific antibodies and chimeric antigen receptor T-cell (CAR-T) therapy, such as Columvi, are used in such cases of relapse. Columvi, the first bispecific antibody to target CD20xCD3 in DLBCL, was launched without reimbursement in Korea in May and is now on the formulary of more than 10 general hospitals. The drug has a 2:1 structure that binds to two CD20 regions on the surface of malignant B cells and one CD3 region on immune T cells, resulting in a stronger binding. Bispecific antibodies have two targets, each targeting a different cell: one that draws immune T cells closer to malignant B cells and the other that activates the T cells to kill the malignant B cells. Based on this mechanism of action, bispecific antibodies have been shown to be effective in patients who are resistant to conventional antibody therapies or chemotherapy. “Bispecific antibodies and CAR-T therapies have been explored as treatment options for DLBCL, but without head-to-head trials, it is difficult to say which is better. The choice of treatment should be based on the individual patient's state of disease progression. However, one of the side effects of CAR-T in elderly patients, immune effector cell-associated neurotoxicity syndrome (ICANS), is considered when selecting a treatment,” said Dr. Fox. He added, “Columvi has a fixed dosing period. It is designed to be administered for up to 12 cycles (8.3 months), so there is a clear end date for the treatment. It also has the advantage of being an off-the-shelf treatment that can be administered to patients immediately.” Columvi achieves 39% CR rate - still effective after 18 months...“justifies the need for its reimbursement” Columvi demonstrated efficacy in the multicenter, open-label Phase I/II NP30179 trial in patients with relapsed or refractory DLBCL after two or more prior systemic therapies. Trial results showed that Columvi achieved a complete response (CR) of 40% and an overall response rate (ORR) of 52%. Among patients who achieved CR, the median duration of response was 26.9 months, with 67% of patients maintaining CR at 18 months. The study also included about one-third of patients who had received prior CAR-T therapy. “Columvi demonstrated a 40% CR rate in the trial, even in patients who are difficult to treat,” said Dr. Fox. This data alone confirms the efficacy of Columvi, as such data cannot be expected with existing standard treatment options, and Columvi is showing similar results in the real world to the clinical trial,” said Dr. Fox. “In DLBCL, relapse typically occurs within 12 to 18 months, and staging progresses rapidly in relapsed patients. We already have data on Columvi’s use in these patients up to 18 months of follow-up. So we can be confident about Columvi’s efficacy data and maintenance of its effect.” However, Columvi’s reimbursement was rejected in July by the Cancer Disease Review Committee, the first gateway to reimbursement in Korea, due to the lack of long-term data. Roche Korea is aiming to reapply for Columvi’s CDDC review later this year. “Patient access to Columvi has been secured in the UK with reimbursement approval,” said Dr. Fox. “This is because the health authorities have recognized Columvi as an effective treatment in DLBCL.” “Columvi is not just an improvement over existing therapies, but a paradigm-shifting treatment for DLBCL. I want to emphasize that this is a treatment that could have an impact on prolonging the survival of patients with relapsed or refractory DLBCL.”

- Company

- Global CDMOs compete to expand ADC capacities

- by Kim, Jin-Gu Nov 14, 2024 05:51am

- Global competition is heating up in the contract development manufacturing organization (CDMO) market for antibody-drug conjugates (ADCs). Major players include Switzerland's Lonza and Samsung Biologics, the world's top two CDMOs, which are competitively expanding their manufacturing facilities. Lonza recently announced the expansion of a 1,200-liter ADC manufacturing facility, while Samsung Biologics announced the start-up of a 500-liter ADC manufacturing facility within the year. According to KoreaBIO, Lonza announced on Dec. 13 (local time) that it plans to add 2 manufacturing facilities in Visp, Switzerland, to expand its 'bioconjugation' service. An additional 1,200-liter manufacturing facility will be built to produce commercial bioconjugates, including ADCs, in high volumes. At the same time, the company will expand the infrastructure of the existing facility. Construction is expected to be completed and the facility fully operational by 2028. The new manufacturing facility will provide comprehensive end-to-end lifecycle support. This includes drug manufacturing for early-stage clinical development, large-scale manufacturing for commercial supply, and finished product filling services. Lonza has been in the bioconjugate CDMO business since 2006. To date, it has produced more than 1,-00 cGMP batches for more than 70 programs. Christian Morello, Vice President, Head of Bioconjugates, Lonza, said, “We continue to see strong growth in the bioconjugates space as ADCs and other bioconjugated drugs increasingly progress towards commercialization. This investment in our multipurpose commercial bioconjugation capacity addresses the growing market demand, enables us to support the growth of our customers, and offers a flexible and integrated service for manufacturing bioconjugates.” The global CDMO market, including Lonza, has recently been intensely competing to expand capacities around ADC drugs. Samsung Biologics is building a dedicated 500-liter ADC manufacturing facility at its Songdo Biocampus in Incheon, South Korea. The company plans to finalize the construction this year and begin full-scale operation after receiving GMP approval. Lotte Biologics is expanding its ADC manufacturing facility at its Syracuse, USA plant. This is an investment of USD 80 million (approximately KRW 100 billion). The ADC manufacturing facility is currently being expanded and is targeting GMP approval in the first quarter of next year. The company is also in the process of building a related plant in Songdo, Incheon. In addition, Celltrion plans to establish a separate CDMO subsidiary while pursuing ADC drug development. Kyongbo Pharmaceutical is investing KRW 85.5 billion to build an ADC plant. The reason why domestic and foreign CDMOs are rushing to expand production capacity for ADC drugs is due to their marketability and high barriers to entry. ADC is a type of antibody conjugated with a cytotoxic drug (payload) as a linker. They have a high structural complexity compared to conventional antibody drugs, which makes the development and manufacturing process difficult, but they have emerged as the next generation of biopharmaceuticals due to their relatively high therapeutic efficacy and low side effects. Following the success of Daiichi Sankyo's breast cancer drug Enhertu (trastuzumab deruxtecan), research on ADC drugs has increased explosively worldwide. However, facilities for the development and mass manufacture of ADC drugs have not been able to keep pace. This is why an imbalance between ADC-related research and manufacturing is expected in the field. Unlike conventional antibody drug CDMOs, ADC-specific manufacturing facilities require more particular technologies. Unlike antibody drug production facilities, ADC production facilities must incorporate additional design principles because they handle cytotoxic drugs (payloads) and organic solvents. Additional design details include negative pressure design, differential pressure between cleanrooms, and airlocks to prevent the spread of cytotoxic drugs and protect operators.

- Company

- Imfinzi combo drug Imjudo can be prescribed at hospitals

- by Eo, Yun-Ho Nov 13, 2024 05:54am

- Immuno-oncology drug Imfinzi's combination partner Imjudo may now be prescribed in general hospitals in Korea. According to industry sources, AstraZeneca Korea's CTLA-4 inhibitor Imjudo (tremelimumab) has passed the drug committees (DCs) of tertiary hospitals in Korea including Seoul National University Hospital and Seoul Asan Medical Center. For now, however, Imjudo is a non-reimbursed drug. AstraZeneca submitted an application for the reimbursement of the PD-L1 inhibitor Imfinzi (durvalumab) and Imjudo combination for liver cancer in June and is currently awaiting a review by the Health and Insurance Review and Assessment Service’s Cancer Disease Review Committee. Imjudo was approved by the Ministry of Food and Drug Safety in combination with Imfinzi in June last year. The first target indication for the combination is liver cancer and can be prescribed as a first-line treatment for adult patients with advanced or unresectable hepatocellular carcinoma (HCC). The specific regimen is the STRIDE (Single Tremelimumab Regular Interval Durvalumab) regimen, which consists of a single dose of Impinj 1,500 mg plus 300 mg of Imfinzi, followed by an additional dose of Impinj at regular intervals every 4 weeks. At the recent European Society for Medical Oncology (ESMO) Congress 2024, the 5-year overall survival data from the Phase III HIMALAYA trial that demonstrated the efficacy of the Imfinzi and Imjudo combination in hepatocellular carcinoma was presented. In the HIMALAYA trial, patients with inoperable HCC were treated with STRIDE (single dose of Imjudo followed by Imfinzi maintenance therapy), Imfinzi monotherapy, and sorafenib monotherapy. When comparing the results of the Imfinzi and Imjudo combination with sorafenib combination therapy in patients with unresectable HCC, patients who received the STRIDE regimen had a 5-year overall survival (OS) rate of 19.6%, compared with the 9.4% for patients who received sorafenib. The median overall survival was 16.43 months and 13.77 months, respectively, showing a 24% lower risk of death in the Imfinzi-Imjudo combination arm. “ The Imfinzi-Imjudo combination therapy has significant advantages in that it has a much lower risk of bleeding than conventional therapies and does not worsen liver function," said Hong Jae Chon, Professor of Hemato-Oncology at CHA Bundang Medical Center. “In particular, the combination shows potential for longer survival than existing therapies."

- Company

- Treatment-refractory Dravet syndrome calls for new options

- by Whang, byung-woo Nov 13, 2024 05:54am

- Despite increased treatment options for the ultra-rare Dravet syndrome, there are still gaps in care that require attention. Even with the introduction of medical cannabis, cannabidiol, there are patients who do not respond to the drug, which is why improving access to new options should be considered. Dravet syndrome is a rare neurological disorder that begins with fever and convulsions within the first year of life, persists into adulthood, and leaves nearly all young patients moderately to severely disabled after each attack. Although it is known to be a rare disease with an estimated prevalence of 1 to 2 per 10,000 people worldwide, there is no officially investigated prevalence in Korea and was designated as an ultra-rare disease in 2022. Dravet syndrome is characterized by the onset of the first seizure, which is similar to a febrile convulsion that usually occurs with fever at 6 months. The biggest risk factor is “Sudden Unexpected Death in Epilepsy” (SUDEP). While the rate of sudden death in intractable epilepsy is 20-25%, in Dravet syndrome, up to 59% of all deaths are associated with SUDEP. The goal of treatment for Dravet syndrome is to control seizure frequency and non-seizure symptoms to reduce the patient's risk of sudden death and improve quality of life. Initial treatment includes anti-seizure medications and add-on treatments such as the anti-seizure medications stiripentol and cannabidiol are used to treat the “drug refractory” nature of Dravet syndrome. Cannabidiol is a medical cannabis preparation that was previously supplied without reimbursement through the Korea Orphan & Essential Drug Center for urgent use but then has been reimbursed since April 2021. Hoon-Chul Kang, professor of pediatric neurology at Severance Hospital, emphasized that the government's approval of medical cannabis has contributed to improving the treatment environment for Dravet syndrome. Kang said, “The government's decision was based on the desperate voices of parents and caregivers of children with Dravet syndrome, as well as objective data reported in the literature,” he explains. Limitations remain for drug-refractory Dravet syndrome...a fundamental solution is needed However, stiripentol and cannabidiol are only available through the Korea Orphan & Essential Drug Center, and the treatment process from applying for the drugs to meeting the criteria for reimbursement coverage is rather complicated. Hoon-Chul Kang, professor of pediatric neurology at Severance Hospital Hoon-Chul Kang, professor of pediatric neurology at Severance HospitalIn particular, there are still many patients with Dravet syndrome who are refractory to existing medications, leaving a blind spot in terms of seizure management. Unlike Korea, where treatment options are limited, options are increasing overseas with the emergence of new options. In the long run, experts agree that Korea also needs a fundamental treatment for seizures that reduces the quality of life for people with Dravet syndrome and their caregivers. If a new treatment option can significantly improve seizure control while also managing additional comorbidities and disabilities, it would substantially improve the treatment landscape. In addition, despite the limitations of being an ultra-rare disease, there are expectations that Dravet syndrome will benefit from the government's 'fast-track program for serious and rare diseases to reduce the burden of medical expenses’ plan. The industry predicts that the government's interest in pediatric rare and intractable diseases will continue for the time being, given the revised pediatric drug pharmacoeconomic evaluation exemption system last year and the selection of drugs for the first pilot project for the approval-evaluation-negotiation linkage system. A professor of pediatrics at a tertiary hospital said, "The government needs to make another timely decision to improve the treatment environment for Dravet syndrome, an extremely rare disease that is even more neglected than others."

- Company

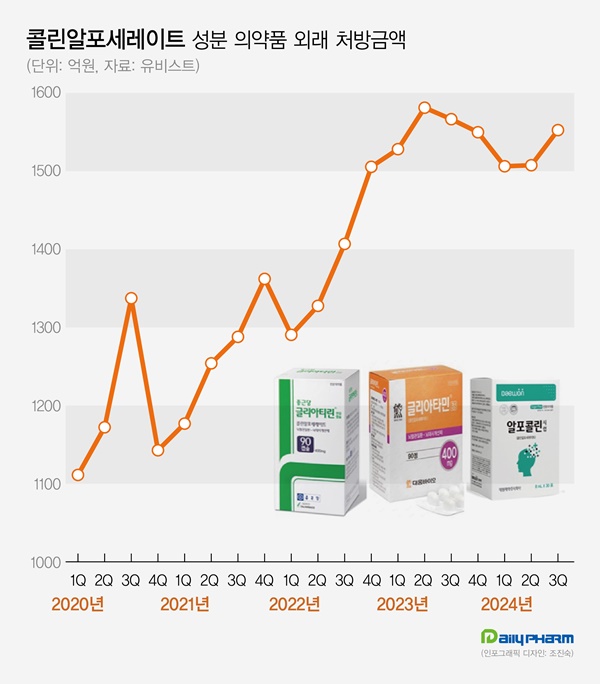

- 'Choline alfoscerate' prescription market continues to grow

- by Chon, Seung-Hyun Nov 13, 2024 05:54am

- The cognitive enhancer 'choline alfoscerate (choline products)' has expanded its presence in the prescription market. Choline products' growth slowed earlier this year but rebounded in Q3, further expanding the market size. Although a few companies withdrew from the market due to the risk of failing clinical re-evaluation, the prescription market continued sales boom. According to the pharmaceutical market research firm UBIST on November 11, the outpatient prescription market for choline products totaled KRW 155.3 billion in Q3. It decreased by 0.9% compared to Q3 of last year but increased by 3.0% compared to the previous quarter. Choline products' prescription sales recorded KRW 158.1 billion in Q2 of 2023. Then they went on a downward slide for three consecutive quarters until Q1 this year. In Q2, the sales slightly increased compared to the previous quarter. In Q3, they showed a strong rebound. Choline products' prescription size for Q3 was recorded as the third highest in history. The slowing growth of choline products in the first half of this year is likely due to steep growth in the past few years. The prescription market for choline products recorded KRW 308.8 billion in 2018. Then, it continued to renew the best record every year. Last year, the market amounted to KRW 622.6 billion, expanding more than twice in five years. Quarterly prescription sales indicate a 46.4% increase over five years from KRW 106.1 billion in Q3 of 2019. Outpatient prescription sales of pharmaceuticals containing choline alfoscerate (unit: KRW 100 million, source: UBIST). Even though choline products are under clinical re-evaluation for efficacy evaluation, clinical practices have continued to have a high demand for choline products. In June 2020, the Ministry of Food and Drug Safety (MFDS) requested companies with choline products to submit their clinical trial documents, and 57 pharmaceutical companies began clinical trials for reassessment. Previously, three indications for choline products had been approved, including ▲secondary symptoms caused by cerebrovascular deficit or degenerative organic brain syndrome ▲emotional and behavioral changes ▲senile pseudodementia. In the re-evaluation process, two out of three indications for choline products were deleted, excluding 'secondary symptoms caused by cerebrovascular deficit or degenerative organic brain syndrome.' Choline products are facing the possibility of reduced reimbursement in addition to the issue of their efficacy. In August 2022, the MOHW issued revised regulations on 'The Criteria and Scope of National Health Insurance,' indicating that patients without prior dementia diagnosis will have a copayment increased from 30% to 80%. After that, two groups of pharmaceutical companies, led by Daewoong Bio and Chong Kun Dang, filed an administrative suit to cancel the MOHW's notification. However, they all lost in the first trial in 2022. Chong Kun Dang also lost in the second trial in May. However, as the suspension of execution filed by pharmaceutical companies has been accepted, reimbursement reductions are on hold. Despite many products being withdrawn from the market after the clinical re-evaluation of choline products, the prescription market continued to grow. According to the MFDS, choline products that received Korean approval total 278 items. Among these, 134 items have been withdrawn from the market due to approval withdrawal or cancelation. Previously, the MFDS ordered the clinical re-evaluation of choline products from 134 companies. 77 companies withdrew from undergoing re-evaluation, resulting in a significant number of withdrawals from the market. More companies that commenced clinical re-evaluation of choline products are withdrawing. In two months from September, Guju Pharmaceutical, Kyongbo Pharmaceutical, PharmGen Science, YooYoung Pharmaceutical, and Medix Pharm voluntarily withdrew choline product approval. Increasing number of companies are exiting the market due to potential retrieval amounts that arise when they fail the re-evaluation for choline products. In 2020, the MOHW issued a national health insurance contract to companies with choline products, entailing 'companies failing clinical trials must return the prescription sales.' Within eight months of the negotiation order, pharmaceutical companies agreed to the term that they would return 20% of the prescription sales from the time they received IND approval to the date of deletion when the indication for the product was deleted due to failed clinical re-evaluation. The retrieval negotiations for choline products are determined by agreements between the MOHW and each pharmaceutical company, resulting in different contract details for each company. While a 20% retrieval rate from prescription sales is commonly applied, the timing of the retrieval rate varies among companies. Sources said that most companies have agreed to increase retrieval rate. For instance, companies may have agreed to set a 10% retrieval rate for this year when they fail the clinical re-evaluation of choline products, then increase to 30% after five years. As the prescription market for choline products continues to grow, companies that agreed to a gradual increase of retrieval rate would end up exponentially expanding retrieval amount due to the market growth. Pharmaceutical companies may have to face increased retrieval amounts as the market for choline products continues to grow if they fail clinical re-evaluation. For these reasons, sources said that more companies are considering exiting the market before completing the clinical re-evaluation. However, analysis suggests that the entire market for choline products continues to grow as other products replace the withdrawn products. Prescription sales by major products indicate that Daewoong Bio's Gliatamin recorded KRW 41.2 billion in Q3, a 4.4% reduction from the previous year. Chong Kun Dang's Chongkundang Gliatirin generated prescription sales of KRW 31.1 billion in Q3, up 10.9% from last year. Arlico's Choliatin recorded prescription sales of KRW 5.1 billion in Q3, a 28.7% reduction from the previous year. Daewon Pharmaceutical's Alfocholine generated prescription sales of KRW 4.9 billion in Q3, down 10.3%. Yuhan's Alfoatilin recorded KRW 3.7 billion, down 16.7% from the previous year. Dongkoo Bio's Glifos' sales increased from KRW 2.7 billion in Q3 of last year to KRW 3.7 billion in a year, up 33.9%. Mother's Pharm's Memoem recorded prescription sales at KRW 1.1 billion in Q3 of last year, then increased to KRW 3.3 billion in a year, an increase of over threefold.

- Company

- Asthma drug 'Monterizine' sales rise despite generic entries

- by Kim, Jin-Gu Nov 12, 2024 05:51am

- Hanmi's asthma treatment, 'Monterizine,' successfully expanded its prescription sales over 10% Year-over-Year (YoY), despite the release of generics. Generic drugs had been listed for reimbursement in October 2023. The analysis suggests that Monterizine's continued sales expansion is because generic prices have not been reduced and, it maintains a strong market presence with its broader scope of use. Prescription sales 14%↑despite generic releases… Monterizine Chewable Tab is the only available treatment for young children According to the pharmaceutical market research firm UBIST on November 8, Hanmi's Monterizine recorded prescription sales of KRW 4.3 billion in Q3, which is an increase of 14% over a year compared to KRW 3.7 billion in Q3 2023. Monterizine is a combination drug containing the asthma treatment, 'Montelukast,' and the third-generation antihistamine, 'Levocetrizine.' Hanmi received approval for 'Monterizine Cap' in May 2017. The following April, Hanmi changed the formulation and received approval for 'Monterizine Chewable Tab' designed to be taken by chewing. After the launch of Monterizine Chewable Tab, prescription sales quickly expanded for the Monterizine series. The combined prescription sales of Monterizine Cap and Monterizine Chewable Tab have increased by 8%, from KRW 7.9 billion in 2019 to KRW 8.6 billion in 2020. It recorded KRW 9.7 billion in 2021, surpassing KRW 10 billion when the sales amounted to KRW 12.4 billion in 2022. Last year, it recorded KRW 15.6 billion, a 21% increase from the previous year. This year, Monterizine is maintaining solid sales. In Q4 2023, it surpassed KRW 4 billion for the first time, generating KRW 4.3 billion to KRW 4.4 billion in sales each quarter. Quaterly prescription sales of the original drug Monterizine (blue) and generics (ligt blue) (unit: KRW 100 million, source: UBSIT). Interestingly, generics of Monterizine were launched in October 2023. Typically, sales of original drug slow down after the generic launches, but Monterizine is following a different trend. The analysis suggests that Monterizine Chewable Tab is showing a strong market presence with its broader scope of use. The scope of use for the original Monterizine Cap and generics to Monterizine are limited to 'adults and adolescents at the age of 15 or older.' Monterizine Chewable Tab is prescribed to 'young children at the age of 6-14.' The analysis is that Monterizine Chewable Tab is widely used in the prescription market, especially because young children require frequent prescriptions in the case of asthma drugs. Drug price has been maintained despite generic releases…the generics formulation is different from the original Additionally, one of the reasons for continued sales of Monterizine is that it remains the same price following the generics' releases. Product photo of HanmiIn September 2021, generics companies challenged four patent cases of Monterizine. In September of the following year, they successfully avoided patents one after another. After losing the first trial, Hanmi appealed to the patent court, but the company soon withdrew. Since October 2023, Monterizine generics have launched. Six products that met the requirement for the highest price by conducting bioequivalence tests became listed at KRW 886 per tablet. 14 products that did not meet the bioequivalence test because they were produced by contract manufacturing organization (CMO) became listed at KRW 753 per tablet. The drug price of Monterizine was not reduced following the generic release. The original drug price is automatically reduced by 30% when generics are released. Monterizine drug price should have been reduced from KRW 886 to KRW 620, but it was not. This is because the generics have been developed in a formulation different from the original. The Health Insurance Review and Assessment Service (HIRA) reduces the original drug price by 30% in the first year when a product with the same formulation is launched. In the following year, the HIRA further reduces the drug price of the original by 53.55%. In this case, the 'same formulation' means the active ingredient, administration route, dosage, administration method, formulation, and efficacy·effects are matched. The original Monterizine is available in capsules and chewable tablets. Generic products received approval as tablets. The government analyzed that the generics are not in the same formulation as the original Monterizine. Therefore, the drug price of the original was maintained at KRW 886.

- Company

- 'Vabysmo' for macular deg associated RVO indication expected

- by Eo, Yun-Ho Nov 12, 2024 05:51am

- Product photo of Vabysmo.The first bispecific antibody for eye diseases, 'Vabysmo,' is soon to be approved in South Korea for its indication of treating macular degeneration associated retinal vein occlusion (RVO). According to industry sources, Roche Korea's Vabysmo (faricimab) is being reviewed by the Ministry of Food and Drug Safety (MFDS) for its indication expansion. It is expected to be approved within the year. For RVO indication, it received the U.S. FDA approval in October 2023. Attention has been drawn to Vabysmo, a treatment for macular degeneration because it significantly extended the administration interval compared to Bayer's 'Eylea (aflibercept), which has been the standard therapy. In South Korea, Vabysmo's prescription became available after it was approved for reimbursement listing for neovascular age-related macular degeneration (nAMD) and diabetes-related macular edema (DME) in October last year. Existing macular degeneration drugs used in South Korea are vascular endothelial growth factor-A (VEGF-A) drugs such as Novartis' 'Lucentis (ranibizumab),' 'Beovu (brolucizumab),' and Eylea. Unlike existing VEGF drugs, like Lucentis and Eylea, Vabysmo can also block the angiopoietin-2 (Ang-2) pathway, thus inhibiting new blood vessel formation. The analysis suggests that blocking two independent pathways can more effectively stabilize blood vessels and reduce inflammation, abnormal vessel growth, and fluid leakage than the VEGF-A pathway alone. RVO is Vabysmo's third indication. Its efficacy has been confirmed through the Phase 3 BALATON and COMOINO studies. In these two clinical trials, Vabysmo achieved non-inferiority in the patient's vision improvement compared to Eylea. When treated with Eylea, the patients had continual vision improvements from the early stage. The safety profile of the trials was similar to previous study reports. Meanwhile, Vabysmo has seen an increase in sales this year. Its sales for Q1 amounted to 847 million francs, up 88.6% from the previous year. It recorded sales of 947 million francs (about 1.51 trillion won) in Q2, up 86.4% from last year. In Q2, Vabysmo surpassed the sales of the market leader Eylea (about 1.26 trillion won) for the first time.

- Company

- Generic companies seek early entry into KRW 100 bil Tagrisso

- by Kim, Jin-Gu Nov 12, 2024 05:51am

- Patent challenges to Tagrisso (osimertinib), a non-small cell lung cancer treatment that posts annual sales of KRW 110 billion, are expanding. The companies that have filed patent challenges seek to first evade the product patent, which expires in 2035, and then launch generics early after November 2033, when the substance patent expires. According to the pharmaceutical industry on the 11th, Kwangdong Pharmaceutical recently filed a passive trial on the scope of rights against AstraZeneca for the Tagrisso formulation patent (10-2336378). The patent expires in January 2035. In addition to the formulation patent, Tagrisso has two other patents listed on the MFDS Green List. They are the product patents (10-1410902-10-1422619) that expire in November and December 2033, respectively. Kwangdong Pharmaceutical plans to launch Tagrisso generics early upon expiration of the substance patent in 2033, having first avoided the product patent, which expires in 2035. It is also possible that the company could further accelerate the early launch by taking advantage of the extended life of the substance patent. Prior to Kwangdong Pharmaceutical, Chong Kun Dang filed a patent evasion trial on Tagrisso’s product patent on the 25th of last month. With Kwangdong Pharmaceutical joining the patent challenge within 14 business days of Chong Kun Dang’s filing, the two companies have secured the “file of initial claims” requirement, which is one of the requirements for obtaining first generic exclusivity rights. Separately, Chong Kun Dang is developing a new drug for the treatment of non-small cell lung cancer. The candidate, CKD-702, has a dual antibody mechanism of action that simultaneously targets cMET and EGFR, and is currently in a global Phase 1 clinical trial. Chong Kun Dang’s strategy is to target the NSCLC treatment market by developing both new drugs and generics. According to the drug market research institution IQVIA, Tagrisso's sales in the Korean market were KRW 111 billion last year. This is up 4% from KRW 106.5 billion it had posted in 2022. The sales are expected to have increased significantly since the drug's reimbursement was expanded to cover “first-line treatment for locally advanced or metastatic NSCLC with certain gene mutations” this year. Leclaza (lazertinib), whose reimbursement was also expanded to first-line treatment along with Tagrisso, generated KRW 22.6 billion in sales last year.

- Company

- Will Lorviqua be reimbursed as a first-line therapy in KOR?

- by Eo, Yun-Ho Nov 11, 2024 05:49am

- Whether progress will be made in the insurance reimbursement discussions for the ALK antitumor drug Lorviqua is gaining attention. The health authorities recently said they would “promptly start discussions” on the need to expand coverage of the ALK-positive NSCLC drug Lorviqua (lorlatinib) to the first-line. Lorviqua is currently in the process of terminating its risk-sharing agreement (RSA) and has applied for a general listing. Pfizer filed for the general listing shortly after the breakdown of drug price negotiations with the National Health Insurance Service in June, but there was little discussion made on the agenda until recently. At the time, the NHIS said that the drugmaker had expressed its intention to switch Lorviqua’s reimbursement listing status to general listing, which was listed through the pharmacoeconomic evaluations exemption system as an expenditure cap type RSA, but that the switching cannot be discussed as the company’s application falls under extending its reimbursed scope of use. As a result, the negotiations broke down. However, despite the company’s prompt reapplication thereafter, this delay in the simple initiation of the process itself has left patients waiting without reservation. However, this time around, the NA’s criticisms have raised hopes for future developments. The issue is in the regulatory process. Currently, RSA drugs can apply for reevaluation upon the expiry of their RSA term, or start their price-volume agreement negotiations from the Health Insurance Review and Assessment Service’s Drug Reimbursement Evaluation Committee’s review stage. However, for RSA drug’s reimbursement extensions, no such streamlined track is available. Moreover, since Lorviqua was originally contracted as an expenditure-cap type RSA drug through the pharmacoeconomic evaluation exemption track but is seeking reimbursement through the general listing track, the government having more difficulty shaping the direction. The problem is that the patients are left to suffer the consequences. Regardless of whether the drug’s reimbursement will be extended or not, the government's flexible administration and the will of the pharmaceutical companies would be needed to achieve results. Yool-Seo Cho, Director of the Korean Lung Cancer Patients' Association, said, “We call on the government to actively improve patient access to treatment, including expediting the review of Lorviqua’s reimbursement, so that patients can receive optimal treatment with less emotional distress and financial burden.” Lorviqua was specifically designed and developed by Pfizer to penetrate the blood brain barrier (BBB). The drug’s high clinical value as a first-line treatment was recognized in the 5-year long-term follow-up results of the CROWN study that was presented at ASCO. Results showed that Lorviqua reduced the risk of disease progression or death by 81% compared to crizotinib, with 60% of patients surviving without disease progression at 5 years. The risk of brain metastasis progression was reduced in 94% of patients, with only 4 of 114 Lorviqua-treated patients without brain metastases developing brain metastases.

- Company

- Companies copromote products at Hypertension Seoul 2024

- by Kim, Jin-Gu Nov 11, 2024 05:49am

- Pharmaceutical and biotech companies with hypertension drugs have gathered at the Conrad Seoul Hotel in Yeouido, Seoul on the 8th. Industry officials, who set up promotional booths at the Korean Society of Hypertension's fall conference (Hypertension Seoul 2024), distributed pamphlets to doctors at the event and introduced the features of their hypertension drugs. The Korean Society of Hypertension held its 2024 Annual Meeting at the Conrad Hotel in Seoul from November 8 to 9. The event was held on the 3rd and 5th floors of the hotel. More than 40 pharmaceutical and biotech companies set up booths at the event. According to the Korean Society of Hypertension, more than 700 healthcare professionals attended this year’s event, and a separate space was prepared to reflect on the society’s history as the society celebrated its 30th anniversary this year. Despite the prolonged strike of doctors that began at the beginning of the year, the total number of participants was similar to that of previous years, said an official from the society. “The number of participants is slightly lower than last year,” the official said, adding, ”I know that other conferences with separate sessions for residents have seen a significant decrease in the number of participants. However, the KSH does not have separate sessions for residents, so there is not much difference.” With so many healthcare professionals attending the event, pharmaceutical companies also eagerly promoted their products at the event. A total of 40 companies set up booths at the event to promote their hypertension drugs. Daewoong Pharmaceutical&Daiichi Sankyo and Boryung&HK inno.N, both Diamond level sponsers, opened the largest booths on the third and fifth floors of the venue. Similarly, the platinum-level participants, Organon Korea, Hanmi Pharmaceutical, GSK, and Yuhan Corp, also set up prominent booths on the third and fifth floors. Notedly, there were booths where two companies were promoting one product at the same time. This is analyzed as a result of the increasing number of co-promotion cases in Korea’s hypertension drug market. Currently, Daewoong Pharmaceutical and Daiichi Sankyo are co-promoting the Olmetec (olmesartan) family, Boryung and HK Inno.N are co-promoting Kanarb (fimasartan) family, Dong-A ST and Celltrion Pharmaceutical are co-promoting Edarbi (azilsartan) family, Handok and Sanofi are co-promoting Aprovasc (irbesartan+amlodipine), and Servier and Kolon Pharmaceutical are co-promoting Acertil (perindopril). Many of these companies organized promotional booths together. For example, Boryung and HK Inno.N set up a large booth at the entrance on the fifth floor of the venue. The two companies had signed a copromotion agreement at the end of last year to jointly market Boryung’s Kanarb Family and HK Inno.N’s K-CAB. As a result, HK inno.N has been conducting sales and marketing activities with Boryung since the beginning of this year, targeting frontline hospitals. Setting up the promotional booth at Hypertension Seoul 2024 was also part of the companies’ copromotion strategy. In particular, the companies put much effort into this event, participating as a Diamond sponsor, which is the highest level, for the first time. Boryung and HK Inno.N jointly installed the booth as well. An official from Boryung said, “We have been jointly selling the Kanarb Family with HK Inno.N starting this year, so we jointly set up a promotional booth at Hypertension Seoul 2024. We expect it to be more effective than promoting alone. This way, I believe we will be able to create synergy by utilizing each company’s respective strengths.” A representative from HK Inno.N said, “This is the first Hypertension Seoul 2024 event that we have participated in since starting copromoting Kanarb. We actively communicated with Boryung before the conference to come up with a strategy. Together with Boryung, we have been introducing domestic clinical cases of fimasartan to physicians visiting our booth.” Daewoong Pharmaceuticals and Daiichi Sankyo also jointly promoted the Olmetec family on the third floor. They focused on the fact that Olmetec Family, which celebrated its 20th anniversary this year, is widely used in hypertensive patients with multiple comorbidities. The companies emphasized the effectiveness of Olmetec in controlling blood pressure in elderly hypertension patients, hypertension patients with diabetes, hypertension patients with obesity, and hypertension patients with cardiovascular disease. A company representative said, “We are conducting various campaigns in celebration of the 20th anniversary of the product this year. Many doctors came to the booth to congratulate and encourage us. We plan to build Olmetec’s next 50 years with these supporters.” Dong-A ST promoted Edarbi, which it is co-marketing with Celltrion Pharmaceutical, at the entrance of the third floor. The company emphasized that the azilsartan ingredient of its drug reduced the mean 24-hour systolic blood pressure change more significantly than valsartan. The booths of solo exhibitors also stood out. Hanmi Pharmaceutical promoted Rosuzet and the Amosarrtan family, emphasizing that they are “the No.1 products. On the second day of the event, the company promoted its products during the Luncheon Symposium. GSK attended the Hypertension Seoul 2024 for the first time this year. But interestingly enough, GSK does not own a separate hypertension product. This is in contrast to other companies that have visited the congress with relevant products, such as antihypertensive monotherapy drugs, antihypertensive-hyperlipidemic combination therapy drugs, or a medical device for blood pressure measurement. Nevertheless, GSK didn't just show up, it became a platinum sponsor, the second highest level of sponsorship, and was given a large booth. Instead, GSK promoted its shingles vaccine, Shingrix. GSK emphasized that patients with cardiovascular disease, who are at higher risk for shingles, should be vaccinated with the American College of Cardiology’s recommended dose of Shingrix. “Studies have shown that people with high blood pressure have twice the risk of shingles than people without other medical conditions,” said a GSK representative. The two conditions have a mutually reinforcing effect, with shingles significantly increasing the risk of cardiovascular disease. We came to the Hypertension Seoul 2024 for the first time this year to actively relay these points to doctors who often see patients with hypertension.” The representative added, “We know that many of the doctors who attend Hypertension Seoul 2024 are practicing physicians, and we hope that through today's event, more doctors will be able to recognize the importance of vaccinating patients with hypertension and cardiovascular disease with Shingrix.”