- LOGIN

- MemberShip

- 2026-04-24 02:52:24

- Company

- Vantive's 1st report since spin-off…renal-focused strategy worked

- by Hwang, byoung woo Apr 15, 2026 08:03am

- Vantive Korea, which spun off from Baxter, disclosed its financial performance since becoming independent through its first audit report.While sales decreased, operating profit doubled, confirming the spin-off's positive effect. This performance indicates that the strategic shift toward a renal-care-centered business led to improved profitability.Notably, the extension of the home-based renal management policy focused on peritoneal dialysis aligns with the company's future business direction and is attracting attention as a medium- to long-term growth driver.First performance since spin-off…improved profitability amid shrinking outer growthVantive was launched in February of last year after spinning off from Baxter's 'Kidney Care and Acute Therapy' business units.According to Vantive Korea's audit report, 2025 sales amounted to approximately KRW 199.7 billion, down from KRW 222.1 billion the previous year.However, the sales decline is due to the timing of the spin-off. While the audit report's fiscal year covers January to December 2025, Vantive Korea was spun off in February of last year, limiting the accuracy of a simple comparison.In fact, sales for Baxter Korea, which included the business unit before the spin-off, increased from KRW 65.0 billion to KRW 91.3 billion. There is an aspect in which the business unit's revenue was split between the two companies, which appears as a decrease.Ultimately, the reduction in outer growth can be interpreted as a fluctuation caused by business restructuring during the division process.In this situation, the key is improving profitability. Vantive Korea's operating profit last year was approximately KRW 7.8 billion, roughly double the KRW 3.7 billion from the previous period. Net income also amounted to approximately KRW 3.0 billion in surplus.This structure shows improved profitability despite reduced outer growth. Gross profit increased, and selling and administrative expenses decreased, leading to expanded operating profit.Unlike 2024, when initial spin-off costs were reflected, the renal-centered structure was fully reflected in 2025.In fact, while discontinued operations' gains and losses were separately reflected in 2024, only performance from continuing operations remained in 2025. This signifies the first complete performance since the spin-off.Vantive Korea's Sales and Operating Profit Changes, (2022-2025) (unit: KRW 100 million). BLUE LINE: Sales, RED LINE: Operating profitFocus on Renal Therapy...Strengthening the Peritoneal Dialysis StrategyAfter a successful spin-off and transition to independence, Vantive Korea is solidifying its identity as a specialist in 'Vital Organ Therapy.'As the number of patients with chronic kidney disease surges amid an aging population, sustained business growth in renal care was one of the major reasons for the spin-off.Against this background, Vantive is currently focusing on providing innovative products to support dialysis at home and in hospitals, digitally enhanced solutions, advanced services, and treatment options to support the renal and vital organ functions of critically ill patients.Among these, the area Vantive is focusing on and strengthening investment in the most is 'Peritoneal Dialysis (PD).' Unlike hemodialysis, which requires patients to visit a hospital three times a week and lie down for 4 hours, peritoneal dialysis allows patients to exchange dialysis fluid themselves at home or at work, maintaining daily life and economic activity.Specifically, Automated Peritoneal Dialysis (APD), in which a machine automatically exchanges dialysis fluid during sleep, is considered a solution that drastically improves a patient's Quality of Life (QoL).The policy environment for peritoneal dialysis is also expected to expand Vantive's influence as it improves.This is because the Ministry of Health and Welfare (MOHW )decided to extend the peritoneal dialysis pilot program, which was scheduled to end last December, by three years. Specifically, the Ministry plans to extend the pilot program by 3 years, until December 2028, and to allocate an additional budget of 75.2 billion KRW.The peritoneal dialysis pilot program began in 2019 and involved 8,881 patients at 80 medical institutions. Registered patients showed results where KRW 130,000 reduced monthly medical expenses per person compared to other patients.Additionally, hospitalization expenses decreased by KRW 390,000, and the number of days stayed was shortened by 0.6 days. The fact that improved efficiency in medical resource utilization was proven led to the extension of the project.Vantive has put forward the expansion of home peritoneal dialysis and digital solutions as core values alongside the spin-off.Growth Potential Amid Policy Variables…Expanding the Market Is KeyOf course, since this is an extension of the pilot stage, several hurdles exist for the peritoneal dialysis market to expand explosively immediately.Given that the medical expense burden is increasing due to the entry into an ultra-aged society, the proportion of home-based medical care is rising, and demand for peritoneal dialysis, which enables economic activity and daily life, is gradually increasing, especially among young patients.Consequently, for Vantive Korea, which can now concentrate its corporate capabilities on the renal therapy field through the spin-off, the government's policy to expand the peritoneal dialysis market inevitably becomes a momentum for company growth.To this end, Vantive Korea is focusing on creating an optimized treatment environment so that patients can proceed with peritoneal dialysis more conveniently at home using digital solutions.Vantive stated that it is making various efforts to increase R&D capabilities at the global headquarters level.Lim Kwang-hyeok, CEO of Vantive Korea, stated, "As a vital organ therapy company, Vantive will continue to collaborate with academic societies and medical staff to create a patient-centered treatment environment and will actively support efforts to expand home-based dialysis."

- Company

- Hanmi to acquire Canadian company Aptose Biosciences

- by Cha, Ji-Hyun Apr 15, 2026 08:03am

- Hanmi Pharmaceutical has effectively completed the acquisition process for Canadian biotech company Aptose Biosciences. Having completed both the shareholder meeting and the final approval process from a Canadian court required to close the deal, the company is expected to fully integrate Aptose as a wholly owned subsidiary as early as the end of this month. Through this acquisition, Hanmi Pharmaceutical plans to secure a North American R&D hub and accelerate the development of global anti-cancer drugs.According to the bio industry on the 14th, Aptose passed the Arrangement Resolution for its acquisition by Hanmi Pharmaceutical’s subsidiary, HS North America, at a special shareholder meeting held on March 31 local time.This comes about 10 days after global proxy advisory firm ISS (Institutional Shareholder Services) officially recommended that Aptose shareholders approve the merger proposal. In its recommendation, ISS positively evaluated the proposed acquisition price as providing a premium over the market price, the absence of competing bids, and the fact that the all-cash consideration structure guarantees shareholders certain liquidity and value realization.As a result of the shareholder vote, 91.5% of all votes cast supported the deal. Even among Minority Shareholders, excluding Hanmi Pharmaceutical and related parties, the proposal passed with a high approval rate of 84.9%.On the same day, the Court of King’s Bench of Alberta also issued its Final Order approving the acquisition agreement. By meeting both the key requirements of shareholder approval and court approval, the acquisition transaction has reached a stage where it is legally enforceable. Hanmi Pharmaceutical and Aptose plan to complete the final payment and delisting procedures by the end of April and incorporate Aptose as a wholly-owned subsidiary of Hanmi Pharmaceutical.The acquisition price is C$2.41 per share. This represents about a 28% premium over the 30-day volume-weighted average price (VWAP) of C$1.88 on the Toronto Stock Exchange (TSX) immediately before the acquisition agreement was signed. The maximum amount required to acquire the remaining shares, excluding the stake already held, is estimated at C$4.925 million (about KRW 5.3 billion). The transaction will be conducted through Hanmi Pharmaceutical’s subsidiary, HS North America, which will acquire all outstanding common shares of Aptose, with the full acquisition consideration paid in cash.Aptose Biosciences’ Pipeline (Source: Aptose)Aptose is a Toronto-based biotech company specializing in new drug development. Founded in 1986 and listed on the Nasdaq in 2014, it possesses an innovative drug pipeline specialized in hematologic malignancies, with its core pipeline being tuspetinib, an acute myeloid leukemia (AML) candidate licensed from Hanmi Pharmaceutical in 2021. At the time, Hanmi Pharmaceutical transferred the rights to tuspetinib to Aptose for a total of up to US$ 407.5 million, including a non-refundable upfront payment of US$ 12.5 million (US$ 5 million in cash and US$ 7.5 million in stock).Tuspetinib is a multi-targeted oral kinase inhibitor that simultaneously inhibits various kinases, such as FLT3 and SYK, and possesses a mechanism of action that demonstrates anticancer activity even in patient groups resistant to existing treatments (such as venetoclax). It is currently undergoing a Phase I/II clinical trial in patients with relapsed or refractory AML. In early clinical trials, tuspetinib reportedly demonstrated meaningful anticancer activity, including complete remission (CR), with objective response rates (ORR) of 30–40% as both monotherapy and combination therapy, along with favorable safety profiles.However, amid a global contraction in biotech investment and a high-interest-rate environment, Aptose encountered financial difficulties. Due to continuous R&D spending, Aptose’s accumulated deficit had reached US$566.43 million by the end of last year, while shareholders’ equity had fallen to negative US$27.17 million, placing the company in a state of complete capital impairment. As independent capital-raising efforts, including a rights offering aimed at resolving the funding crisis, repeatedly fell through, its share price continued to decline. Ultimately, the company failed to meet the requirements for maintaining its NASDAQ listing and was delisted in April of last year.Against this backdrop, Hanmi Pharmaceutical continued to provide support as a strategic investor. Hanmi has invested more than US$41 million in the development of tuspetinib and, in November last year, signed an agreement to acquire all remaining shares, thereby solidifying its direction toward full acquisition. It is understood that Hanmi Pharmaceutical made the final decision to acquire the company after comprehensively considering the clinical potential of tuspetinib and the need to secure an R&D hub in North America. Hanmi is effectively spending more than KRW 60 billion in total to acquire Aptose.Once the Aptose acquisition is completed, Hanmi Pharmaceutical is expected to speed up its entry into the North American market in earnest. The company’s strategy is to secure local clinical and research bases in North America while strengthening its oncology pipeline centered on tuspetinib, thereby enhancing its global anticancer drug development capabilities. Through this, the company expects to establish a value chain spanning from global clinical trials to commercialization.

- Company

- Leukemia drug Vanflyta enters market

- by Son, Hyung Min Apr 15, 2026 08:03am

- With the domestic approval of ‘Vanflyta,’ a targeted therapy for FLT3-ITD mutation-positive acute myeloid leukemia (AML), the possibility of a shift in treatment strategies is being raised.Not only has a treatment option covering the full course from combination use in induction and consolidation therapy to maintenance therapy been added, but the drug is also expected to emerge as a new alternative for patients at high risk of relapse after demonstrating clinical benefits such as improved overall survival (OS).On the 14th, Daiichi Sankyo Korea held a press conference at the Plaza Hotel in Jung-gu, Seoul, to commemorate the domestic approval of Vanflyta (quizartinib). Vanflyta was approved in Korea in January for the treatment of acute myeloid leukemia (AML).Professor Byung Sik Cho, Department of Hematology, Seoul St. Mary’s HospitalThe specific indication includes its use for newly diagnosed adult AML patients who are positive for the FLT3-ITD mutation, in combination with standard cytarabine- and anthracycline-based induction therapy and cytarabine consolidation therapy, and as monotherapy maintenance treatment thereafter.Its defining feature is its applicability to a full-cycle treatment strategy spanning induction, consolidation, and maintenance.With this approval, a new FLT3-targeted therapy has been added to the AML treatment landscape, alongside Novartis’ ‘Rydapt (midostaurin)’ and Astellas’ ‘Xospata (gilteritinib).’Experts agree that the arrival of Vanflyta is particularly significant as it offers a treatment option specifically targeting FLT3-ITD mutation-positive patients, who remain at high risk of relapse despite existing treatment.FLT3 mutations are detected in approximately 37% of newly diagnosed AML patients, with about 80% of these cases involving the FLT3-ITD mutation. This mutation is known to promote cancer cell proliferation and increase the risk of relapse, and the 5-year survival rate for these patients is only about 20%.FLT3 is a key receptor that regulates the survival, proliferation, and differentiation of hematopoietic stem cells; however, when a mutation occurs, abnormal signaling is activated, promoting the growth of leukemia cells.Professor Byung Sik Cho of the Department of Hematology at Seoul St. Mary’s Hospital said, “Treatment outcomes have improved since the introduction of FLT3-targeted agents, but even when existing FLT3 inhibitors are combined with chemotherapy, relapse rates of around 40% are still reported. There has been a significant unmet need for new treatment options that can improve outcomes, especially in FLT3-ITD-positive patients.”Vanflyta demonstrated efficacy in the Phase III QuANTUM-First study in patients with FLT3-ITD mutation-positive AML. In the study, patients were randomized 1:1 to the Vanflyta group or the placebo group, received combination treatment with induction and consolidation therapy, and then underwent maintenance therapy for up to 3 years.Dong-Yeop Shin, Division of Hematology and Medical Oncology, Seoul National University HospitalThe results showed that the Vanflyta group’s risk of death was reduced by 22% compared to the placebo group. At a median follow-up of 39.2 months, the median overall survival (OS) was 31.9 months in the Vanflyta group, more than double the 15.1 months observed in the placebo group.Additionally, the duration of complete remission (CR) was 38.6 months in the Vanflyta group, approximately 3 times longer than the 12.4 months in the placebo group, demonstrating meaningful improvement in disease control as well.In terms of safety, febrile neutropenia, hypokalemia, and pneumonia were reported as major adverse events, and the overall pattern of adverse events was similar to that of the placebo group.Professor Dong-Yeop Shin of the Division of Hematology and Oncology at Seoul National University Hospital said, “Vanflyta demonstrated consistent benefits not only in improving overall survival but also in prolonging the duration of complete remission and reducing the cumulative relapse rate. It has the potential to change the treatment paradigm for FLT3-ITD mutation-positive AML.”

- Company

- Huinno focuses on 'ECG monitoring device,' boosting monitoring competitiveness

- by Hwang, byoung woo Apr 14, 2026 12:04pm

- As the wearable patient monitoring market competition is centered around functional expansion, Huinno has unveiled a ward monitoring strategy focused on electrocardiogram (ECG) monitoring.Yeongjoon Gil, CEO of HuinnoOn the 10th, Huinno held a briefing to unveil its smart AI telemetry system, 'MEMO Cue,' emphasizing its safety features, including defibrillation protection circuits, AI interpretation technology, and a structure linked to health insurance reimbursement, as its competitive edge in ward monitoring.Existing ward patient monitoring devices are primarily wire-based. Patients must be attached to various sensors and cables, creating a structure that limits movement. This has been repeatedly pointed out for increasing fall risks, causing patient discomfort, and placing a management burden on medical staff.MEMO Cue addresses these issues with a chest-attached patch-based wearable ECG device. Using an ultra-lightweight patch weighing approximately 9g, patients can move freely while their ECG, respiration rate, and oxygen saturation are monitored in real time.Hospitals can remotely check multiple patients simultaneously through an integrated control system. The company explained that operational efficiency can be improved through a central monitoring system rather than the traditional approach of checking directly at the patient's bedside.In particular, increasing alarm accuracy and reducing false alarms were presented as major differentiators.CEO Yeongjoon Gil explained, "Existing equipment has many false alarms, so medical staff sometimes turn them off," adding that "MEMO Cue is focused on increasing alarm accuracy and reducing medical staff fatigue by applying learning-based AI."The explanation is that in clinical tests, an overall accuracy of approximately 98.5% was achieved, and the alarm precision indicator also exceeded that of competitive products worldwide.Emphasis on Defibrillation Protection Design... Differentiating Patient SafetyDuring the briefing, Huinno emphasized the defibrillation protection design.Defibrillators used in the treatment of cardiac arrest patients deliver high-voltage energy of up to 360J. General wearable ECG devices may be destroyed by this impact or pose a secondary risk to the patient.Huinno explained that MEMO Cue can operate normally even under the same conditions by applying a defibrillation protection circuit. In a field demonstration, while devices without a protective design were damaged, MEMO Cue maintained a normal signal after impact.MEMO Cue met the international medical device safety standard IEC 60601-1 and obtained the electrical grade 'Type CF Defib-proof.' FDA 510(k) approval is also in progress.Regarding this, CEO Gil explained that the defibrillation protection design is significant not only for patient safety but also for hospital operations. This is because equipment without a protective design must be removed in an emergency, but equipment with a protective design allows for continuous monitoring.CEO Gil stated, "Monitoring must be continuously possible without removing the equipment, even in a cardiac arrest situation," and added, "There is a need for ward monitoring equipment designed on the premise of patient safety."For MEMO Cue, both technical strength and the insurance reimbursement structure were emphasized. The product received the remote heart rate monitoring fee (EX871) from the Health Insurance Review and Assessment Service (HIRA), and it can be prescribed concurrently with existing Holter test fees.It was explained that hospital entry burdens can be reduced by performing real-time monitoring and post-analysis simultaneously with a single device.Huinno also presented integration with its existing ECG analysis service, 'Memo Care,' as a strength. It has been designed to conduct automated analysis reports based on data collected during ward monitoring.CEO Gil said, "We are building a platform that covers the entire medical lifecycle from diagnostic assistance and real-time monitoring to prediction. Our goal is to secure global competitiveness in the AI-based patient monitoring market."Early Stages of the Ward Monitoring Market...ECG-Centered Competition Begins in EarnestHuinno concluded that the wearable ward-monitoring market is in its early stages and that competition is rapidly expanding.The current number of beds in Korea subject to ECG monitoring is approximately 500,000. It was analyzed that the entire market has formed, including approximately 50,000 beds in advanced general hospitals, approximately 120,000 beds in general hospitals, nursing hospitals, and primary medical institutions.However, Huinno pointed out that competition is flowing toward simple functional expansion.CEO Gil said, "Recently, competitors have been emphasizing the expansion of various vital signs such as oxygen saturation, blood pressure, and body temperature, but the essence of the current fee is ECG monitoring," and that "Without ECG monitoring, it is difficult to bill for medical acts with other vital signs alone."Huinno's technology competitiveness: a chest-attached patch-based wearable ECG device; wearable lightweight design; AI-based false alarm reduction; defibrillation protection design; Holter record integration; Huinno's MEMO Cue received the remote heart rate monitoring fee (EX871) from the Health Insurance Review and Assessment Service (HIRA). (source: presentation)In other words, the recent view is that the core competitive axis of the wearable patient monitoring market is still ECG-based accuracy and reliability.Huinno plans to maintain its competitiveness in the ward monitoring market by leveraging its experience securing a high market share in advanced general hospitals through its existing Holter analysis service, MEMO Care. The company explained that the service has secured approximately 60% of the market share, based on HIRA data.Additionally, as differences from competitive products, the company presented ▲wearable lightweight design ▲AI-based false alarm reduction ▲defibrillation protection design ▲Holter record integration.Finally, CEO Gil added, "It is the beginning stage of the wearable ward monitoring market opening. We will compete with major global players with a product that ensures both hardware safety and AI software accuracy."

- Company

- Nemluvio forms a new pillar in dermatitis treatment

- by Son, Hyung Min Apr 14, 2026 08:53am

- The arrival of a biologic with a new mechanism of action in the treatment fields of atopic dermatitis and prurigo nodularis is raising the possibility of a shift in treatment strategies.In particular, ‘Nemluvio (nemolizumab),’ which directly blocks IL-31 signaling in these two conditions where severe itching is a key symptom, is expected to emerge as a new treatment option based on its rapid symptom-relief effect.On the 13th, Galderma Korea held a media session at the Plaza Hotel in Jung-gu, Seoul, to commemorate the domestic approval of the biologic Nemlubio.Nemluvio media sessionNemluvio is a monoclonal antibody that inhibits the IL-31 signaling pathway, which is considered a major driver of itch. It received approval as a treatment for atopic dermatitis and prurigo nodularis in Korea last January. Among biologics targeting these diseases, Nemluvio is the first IL-31 inhibitor.IL-31 is known to be a key pathway in the ‘itch-scratch cycle,’ directly stimulating sensory nerves to transmit itch signals and triggering repetitive scratching behavior. Furthermore, it is identified as a major factor exacerbating the disease through a complex mechanism involving inflammatory responses, epidermal barrier dysfunction, and skin fibrosis.Nemluvio demonstrated statistically significant itch relief compared to the placebo group within 48 hours of administration in both atopic dermatitis and nodular prurigo patients. Additionally, when used in combination with topical corticosteroids (TCS) or topical calcineurin inhibitors (TCI), it met all primary endpoints.Specifically, in atopic dermatitis, the proportion of patients achieving at least a 75% improvement in the Eczema Area and Severity Index (EASI-75) was significantly higher than in the placebo group. In prurigo nodularis, at week 16, the proportion of patients achieving an Investigator’s Global Assessment (IGA) score of 0/1, meaning ‘clear or almost clear’ skin lesions, was more than three times higher than in the placebo group.Professor Jung Eun Kim, Department of Dermatology, Catholic University of Korea, Eunpyeong St. Mary's HospitalThe long-term follow-up studies also showed sustained efficacy and safety. According to interim analyses of the long-term extension studies in atopic dermatitis (ARCADIA LTE, 104 weeks) and prurigo nodularis (OLYMPIA LTE, 100 weeks), the improvements observed in skin lesions, itch, sleep, and overall quality of life remained consistent for more than 2 years, with no new adverse reactions observed.Based on this evidence, combination therapy with Nemluvio was also included in the 2025 U.S. atopic dermatitis treatment guidelines.Jung Eun Kim, Professor of Dermatology at Catholic University of Korea Eunpyeong St. Mary's Hospital, said, “Among approved biologics, Nemluvio showed the fastest effect in improving itch. It also offers safety advantages, as no increase in side effects like conjunctivitis, which has been a concern with existing treatments, was observed.”She continued, “The proportion of moderate-severity patients with atopic dermatitis is increasing compared to severe cases. This is especially meaningful as a treatment option in elderly patients, where safety is particularly important.”Galderma Korea plans to launch Nemluvio in the second half of this year and has already applied for reimbursement listing.Jai Hyuck Lee, General Manager of Galderma Korea, said, “Nemluvio directly inhibits IL-31, a key trigger of itch, and is expected to present a new treatment paradigm for patients who face limitations with existing therapies.”

- Company

- Obesity·COVID-19 drugs change multinational pharma performance

- by Son, Hyung Min Apr 14, 2026 08:53am

- There was no outstanding player. The performance of multinational pharmaceutical companies' Korean subsidiaries last year diverged sharply by product portfolio.While some companies recorded high growth driven by expanded obesity treatments, those that saw sales boosts from COVID-19 showed a clear downward trend in growth following the transition to the endemic phase.According to the Financial Supervisory Service on the 14th, sales by the Korean subsidiaries of 30 major multinational pharmaceutical companies increased by 8.0% from KRW 8.7417 trillion in 2024 to KRW 9.4453 trillion last year. Among the 30 Korean subsidiaries, revenue increased for 24 companies, including Novartis Korea, Novo Nordisk, Sanofi-Aventis Korea, and AstraZeneca Korea.Novartis Korea recorded the highest sales among the Korean subsidiaries of multinational pharmaceutical companies. The company's sales last year amounted to KRW 721.3 billion, up 6.3% from the previous year.In terms of operating profit, Otsuka Korea was the highest. Otsuka Korea recorded an operating profit of KRW 49.9 billion last year, a 6.2% increase from KRW 47.0 billion in 2024.Janssen Vaccine recorded sales of KRW 78.4 billion last year, a sharp 52.7% increase from KRW 51.3 billion in the previous year.However, the company faced changes in terms of business continuity. According to the public disclosure, the management of the parent company of Janssen Vaccine decided to cease business activities in November 2025, and last year's financial statements were prepared on a liquidation basis without applying the going-concern assumption.Accordingly, despite the increase in sales, Janssen Vaccine continues to reflect uncertainty about the continuity of its future business.Sales Trend of Multinational Pharmaceutical Companies' Korean Subsidiaries: (from top) Novartis Korea, Novo Nordisk, Sanofi-Aventis Korea, AstraZeneca Korea, Pfizer, MSD Korea, Merck, Roche Korea, Eli Lilly Korea, Janssen Korea, GSK, Viatris Korea, AbbVie Korea, Boehringer Ingelheim Korea, Bayer Korea, Otsuka Korea, BMS Korea, Amgen Korea, Gilead Sciences Korea, Janssen Vaccine, Lundbeck Korea, Ferring Korea, UCB Korea, Menarini Korea, Ipsen Korea, BeOne Medicines, Teva Handok, Leo Pharma, and Kyowa Kirin Korea.Major shifts with obesity drugs… Explosive growth for Lilly and Novo NordiskCompanies selling obesity drugs posted the highest growth rates.Eli Lilly Korea's sales last year was KRW 482.1 billion, a 193.6% increase from the previous year. Operating profit also surged 259.2%, from KRW 10.3 billion to KRW 37.1 billion. Eli Lilly Korea showed the highest sales growth rate among major multinational companies.Previously, Lilly maintained stable sales with oncology drugs such as 'Verzenio (abemaciclicb)' and 'Cyramza (ramucirumab),' as well as the SGLT-2 inhibitor 'Jardiance (empagliflozin)' and the biological agent 'Taltz (ixekizumab),' but it showed a stagnant trend, recording approximately KRW 200 billion sales from 2021 to 2024.This structure changed completely after the launch of the obesity treatment 'Mounjaro (tirzepatide).' Mounjaro, launched in Korea last August, quickly settled in the market, becoming a core growth pillar in a short period.According to the market research firm IQVIA, Mounjaro surged from KRW 28.4 billion in the third quarter of last year to KRW 187.1 billion in the fourth quarter, surpassing KRW 100 billion in quarterly revenue for a single product. Market presence was expanded by overtaking the competing drug 'Wegovy (semaglutide).'This demand expansion was reflected directly in the financial indicators. Eli Lilly Korea's inventory assets increased by 279.3% from KRW 49.4 billion to KRW 187.3 billion, and cash and cash equivalents also increased by 88.6% from KRW 82.1 billion to KRW 154.8 billion. This reflects both the improvement in cash generation following the revenue expansion and a strategy to preemptively secure volume.Novo Nordisk gained effects from 'Wegovy (semaglutide).' The company's sales increased by 85.6% from KRW 308.5 billion to KRW 613.6 billion, and operating profit also increased by 77.1% from KRW 13.7 billion to KRW 24.2 billion.Novo Nordisk, which had maintained stable growth centered on insulin, hemophilia treatments, and Saxenda, saw its performance structure change completely after the launch of Wegovy.Last year, Wegovy's revenue was KRW 467.0 billion, accounting for more than 70% of the total, creating an unusual structure where a single product led the growth of the legal entity. Every quarter, it showed rapid market dominance, surpassing KRW 100 billion in revenue within one year of its launch.Companies with COVID-19 boost see sales decrease… Kyowa Kirin -80% following business saleCompanies that relied on the special boost from COVID-19 entered a clear phase of negative growth following the transition to the endemic phase.MSD Korea's sales decreased 14.2% from KRW 667.8 billion in 2024 to KRW 573.2 billion last year. During the same period, operating profit decreased 13.0% from KRW 24.9 billion to KRW 21.6 billion.The main reason for the sales decrease was the supply void of the COVID-19 treatment 'Lagevrio (molnupiravir).' MSD Korea explained that the absence of a supply contract with the Korea Disease Control and Prevention Agency last year affected the revenue decrease.In fact, MSD Korea's sales have been highly volatile, driven by demand for COVID-19 treatments. Revenue peaked at KRW 820.4 billion in 2022 when demand reached its peak, but subsequently decreased to KRW 760.9 billion in 2023 and KRW 667.8 billion in 2024 following the endemic transition. Compared with last year's revenue of KRW 573.2 billion, revenue has shrunk by 30.1% over the past three years.While performance decreased due to the revenue shortfall from COVID-19 treatments, MSD Korea is seeking a rebound by reorganizing its portfolio around oncology, vaccines, and rare diseases.Pfizer Korea showed a similar trend. The company's sales decreased 25.2% from KRW 783.7 billion in 2024 to KRW 586.1 billion last year.The company's overall performance shrank as demand for the COVID-19 vaccine 'Comirnaty' and the treatment 'Paxlovid' plummeted. This is the result of reflecting the base effect from the significant decrease in public supply volume, which had surged during the pandemic.Gilead also saw sales decrease 26.8% from KRW 319.8 billion in 2024 to KRW 234.0 billion last year due to the supply void of the COVID-19 treatment 'Veklury.'For Kyowa Kirin Korea, the sales decline continued due to the sale of its business. The company's sales last year amounted to KRW 13.8 billion, a sharp 79.9% decrease from the previous year.Kyowa Kirin Korea sold its Asia-Pacific business unit after conducting a restructuring in Korea in 2024. The company sold its China business to Hong Kong's Winhealth Pharma Group. Kyowa Kirin Korea transferred its promotion and distribution units in major Asian countries, such as Korea and Taiwan, to the pharmaceutical distributor DKSH.In addition, sales decreased slightly for Amgen Korea (-6.2%) and Teva Handok (-3.9%).

- Company

- Final Zemiglo use patent invalidated in Korea

- by Kim, Jin-Gu Apr 13, 2026 09:11am

- The dispute surrounding the use patent for LG Chem’s diabetes treatment Zemiglo (gemigliptin) has ended with a final victory for generic companies. With this ruling, generic companies will be able to launch generic versions of Zemiglo after the substance patent expires in January 2030.Supreme Court issues discontinuance of trial on LG Chem’s appeal… use patent finally invalidatedAccording to the industry sources on the 10th, the Supreme Court issued a discontinuance of trial in the final appeal of the Zemiglo use-patent invalidation case filed by LG Chem against Celltrion Pharm, Dongkoo Bio & Pharma, Daehwa Pharmaceuticals, Jeil Pharmaceutical, and Boryung.A discontinuance of trial means that the Supreme Court affirms a lower court’s ruling without reviewing the merits of the case, having determined that the grounds for the appeal do not meet legal requirements. Consequently, the second-instance ruling, in which LG Chem lost, has been finalized. The use patent for Zemiglo has therefore been invalidated.LG Chem and generic drug companies had been in dispute over the use patent, which expires in October 2039. This patent covers the combined administration of gemigliptin and insulin. Celltrion Pharm and others filed a petition for invalidation in 2023, arguing that the patent lacked inventive step.The Intellectual Property Trial and Appeal Board (first instance) and the Intellectual Property Court (second instance) both ruled in favor of the generic companies. The Supreme Court then reached the same conclusion, putting an end to a legal battle that had lasted nearly 3 years.Impact of the final invalidation ruling… scope-confirmation litigation previously won by LG Chem also heading toward closureThis ruling is expected to influence a separate litigation regarding the scope of rights currently underway concerning the same use patent.Until now, disputes over Zemiglo’s use patent had proceeded along two separate tracks - the ‘invalidity lawsuit’ and the ‘scope of rights confirmation lawsuit.’ While the generic company won both disputes in the first instance, the rulings diverged in the second instance. While the generic drug companies prevailed in the invalidity suit regarding the use patent, the original manufacturer, LG Chem, won the dispute over the scope of rights.Because of those conflicting second-instance rulings, uncertainty grew over the timing of the early generic launch. At the time, there were concerns that if LG Chem ultimately succeeded in defending the patent, a generic launch could be delayed until after 2039.However, the situation has now reversed with the Supreme Court ruling. Legally, once a patent is definitively invalidated, the rights associated with it are deemed to have never existed from the outset. That means the favorable ruling LG Chem obtained in the scope-confirmation litigation loses legal effect, because the patent in question, which served as the basis for comparison, is now interpreted as “non-existent.”From the perspective of generic drug companies, this ruling effectively allows them to bring forward the launch of Zemiglo generics by 9 years, to a date after January 2030, when the substance patent expires. Although Zemiglo has a salt and hydrate patent set to expire in October 2031, generic drug companies have already successfully circumvented it.Zemiglo is LG Chem’s flagship drug. According to market research firm UBIST, the combined prescription sales of the ‘Zemiglo family’, which includes Zemiglo, Zemimet, Zemidapa, and Zemiro, totaled KRW 159.1 billion last year, a 4% increase from the previous year. Among these, Zemiglo alone recorded KRW 41.4 billion in prescription sales, accounting for 26% of the total family product prescriptions.

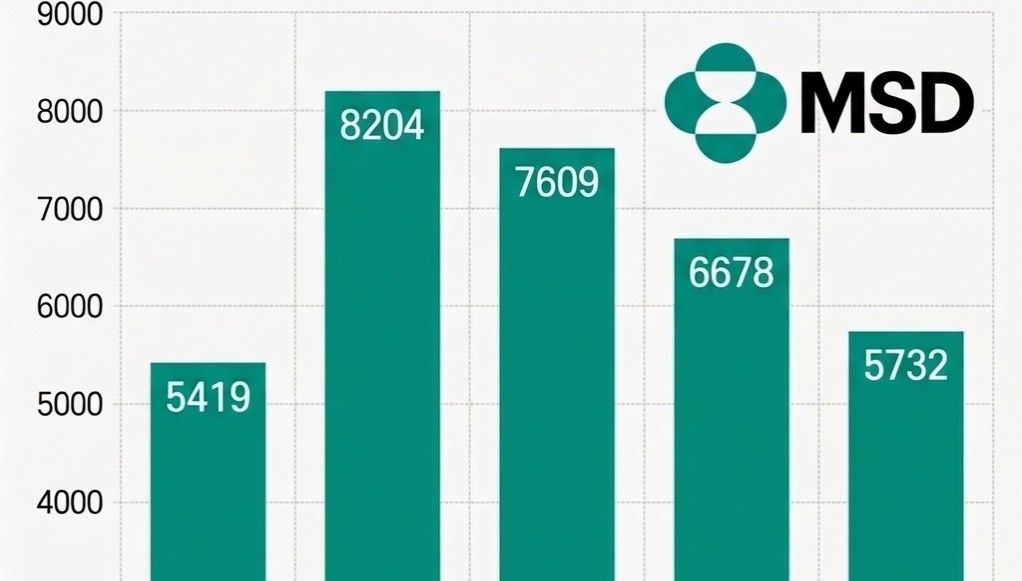

- Company

- MSD Korea sales 30%↓ in three years

- by Son, Hyung Min Apr 13, 2026 09:11am

- MSD Korea's performance continued to decline due to lower demand for COVID-19 treatments. As sales from treatments that drove performance during the pandemic have rapidly shrunk, existing core products have failed to offset the loss.According to the Financial Supervisory Service's electronic disclosure system on the 13th, MSD Korea's sales decreased by 14.2%, from KRW 667.8 billion in 2024 to KRW 573.2 billion last year. During the same period, operating profit dropped 13.0%, from KRW 24.9 billion to KRW 21.6 billion.MSD Korea Sales Trend by Year (unit: KRW 100 million). MSD Korea's sales decreased by 14.2%, from KRW 667.8 billion in 2024 to KRW 573.2 billion in 2025.The primary reason for the sales decline is the lack of supply of the COVID-19 treatment 'Lagevrio (molnupiravir).' MSD Korea explained that the absence of a supply contract with the Korea Disease Control and Prevention Agency (KDCA) last year affected the sales decrease.In fact, MSD Korea's sales have shown significant volatility, reflecting demand for COVID-19 treatments. Revenue peaked at KRW 820.4 billion in 2022 when demand was the highest, but subsequently decreased to KRW 760.9 billion in 2023 and KRW 667.8 billion in 2024 following the transition to the endemic phase. Compared with last year's sales of KRW 573.2 billion, revenue has shrunk by 30.1% over the past three years.Despite having a strong lineup of major products, including the immunotherapy 'Keytruda (pembrolizumab),' the cervical cancer vaccine 'Gardasil,' and the pneumococcal vaccines 'Vaxneuvance' and 'Capvaxive,' it was not enough to fill the void left by the end of the COVID-19 sales.However, the company continued investing in its Research and Development (R&D).According to data released by MSD Korea, the company invested 78 billion KRW in R&D last year, accounting for approximately 14% of its revenue, and has consistently invested over KRW 70 billion annually for the past five years. Despite the short-term performance decline, the company appears to be continuing its strategic investments to secure a foundation for medium- to long-term growth.New Indications·Pipeline Additions…Seeking a Rebound in PerformanceWhile performance has declined due to the sales void from COVID-19 treatments, MSD Korea is seeking a rebound opportunity by reorganizing its portfolio around oncology, vaccines, and rare diseases.The scope of Keytruda was rapidly expanded this year, with 11 additional indications, including triple-negative breast cancer and endometrial cancer, added to the reimbursement list. Furthermore, reimbursement for combination therapy with 'Padcev (enfortumab vedotin)' in urothelial carcinoma is also imminent.RSV preventive antibody injection 'Enfloncia (clesrovimab)' Keytruda has become a pillar of treatment with expanded reimbursement scope as a standard of care (SOC) across major solid tumors. This treatment has the most indications among drugs authorized in Korea.At the same time, efforts to develop new growth engines for infectious diseases are underway. MSD Korea has applied for the authorization of 'Enfloncia (clesrovimab),' an RSV preventive antibody injection for neonates and infants, and there is talk of possible approval in the second half of this year.Enfloncia is a long-acting monoclonal antibody that, in Phase 2b/3 clinical studies, demonstrated reductions of 60.5% in the occurrence of RSV-related lower respiratory tract infections and 84.3% in the risk of hospitalization.In addition, the reimbursement process for 'Winrevair (sotatercept),' a treatment for pulmonary arterial hypertension (PAH), is accelerating following its inclusion in the pilot project for concurrent authorization, evaluation, and negotiation.Winrevair is the first approved activin signaling inhibitor (ASI) in pulmonary arterial hypertension and offers a new mechanism of action after 20 years. This treatment works by blocking excessive activin signaling. This protein complex promotes cell proliferation in pulmonary arterial vessels, and restores the balance with anti-proliferation signals to induce reverse remodeling, normalizing altered vascular structures.As the impact from the termination of the COVID-19 special demand is being reflected, the expanded reimbursement for major products and the introduction of new drugs are expected to be key drivers of a future performance rebound.

- Company

- AZ launches Tezspire in Korea with expanded indication

- by Son, Hyung Min Apr 10, 2026 08:27am

- AstraZeneca Korea (CEO Eldana Sauran) announced on the 8th the domestic launch of Tezspire (tezepelumab) as an add-on maintenance treatment for severe asthma and chronic rhinosinusitis with nasal polyps (CRSwNP).With this domestic launch, Tezspire has simultaneously expanded its indication to include its use as an add-on maintenance treatment for adults with inadequately controlled CRSwNP, broadening its use as an anti-TSLP (Thymic Stromal Lymphopoietin) treatment option for severe asthma to CRSwNP.TSLP is a driver of multiple inflammatory responses and is expressed at higher levels in CRSwNP patients than in patients without polyps. Tezspire is an anti-TSLP monoclonal antibody that blocks TSLP activity at the upstream level of inflammatory pathways. Tezspire’s clinical efficacy and safety profile were confirmed in the global Phase III WAYPOINT trial.The WAYPOINT study was a multicenter, randomized, double-blind, placebo-controlled Phase III clinical trial conducted in 10 countries involving 408 patients aged 18 years and older with CRSwNP who had severe, uncontrolled symptoms.Results showed that at Week 52, the Tezspire treatment group demonstrated statistically significant improvements compared to the placebo group, with a decrease of -2.07 in the Nasal Polyps Score (NPS), which assesses the size and extent of nasal polyps, and a decrease of -1.03 in the Nasal Congestion Score (NCS), which assesses the degree of nasal congestion. Furthermore, these improvements were observed as early as week 4 and week 2 of treatment, respectively, and were sustained through week 52.Ji-young Kim, Executive Director of AstraZeneca Korea’s Respiratory Division, said, “We are pleased that we were able to expand Tezspire’s indication in Korea following FDA approval in October last year for CRSwNP. Clinical trials confirm Tezspire can be an effective treatment option not only for asthma but also for patients with CRSwNP, and we expect it to help patients manage their respiratory conditions.”Rhinosinusitis is characterized by two or more symptoms, including nasal congestion, nasal obstruction, or a runny nose, and becomes chronic when these symptoms persist for 12 weeks or longer. Additionally, when accompanied by nasal polyps, it is classified as CRSwNP.

- Company

- Boston Scientific Korea’s sales surpass ₩200 billion

- by Hwang, byoung woo Apr 10, 2026 08:26am

- Boston Scientific Korea has surpassed KRW 200 billion in sales following portfolio restructuring.Analysts attribute this revenue expansion to the robust growth of the Pulse Field Ablation (PFA) system, coupled with concurrent growth across all major therapeutic areas.According to a recent audit report, Boston Scientific Korea posted KRW 218.5 billion in sales in 2025, up 18.4% from KRW 184.6 billion the previous year.This marks the first time the company has surpassed KRW 200 billion in revenue since entering the Korean market, continuing its four-year growth streak from KRW 151.6 billion in 2022, KRW 175.3 billion in 2023, and KRW 184.6 billion in 2024.Operating profit also grew in tandem with topline growth, from KRW 9 billion in 2022, KRW 10.5 billion in 2023, KRW 11 billion in 2024, to KRW 13 billion in 2025.Increased PFA procedures for arrhythmia drive growthThe key driver behind the company’s growth lies in changes to the business portfolio. The product lines currently supplied by the company to domestic medical institutions span the cardiovascular, oncology, and urology fields. After previously attempting to enter the structural heart disease segment with TAVI before discontinuing the business, the company restructured its portfolio.Representative products include the AVIGO Plus coronary ultrasound imaging device, the TheraSphere liver tumor embolization device, and the Rezum system for benign prostatic hyperplasia.Among these various products, the PFA system had the greatest impact on growth last year.Unlike conventional radiofrequency ablation or cryoballoon ablation, PFA selectively destroys myocardial cells only, reducing procedure time by more than half and lowering complication risks, thereby expanding its influence in major domestic general hospitals.The Korean PFA market is currently contested by Boston Scientific, Medtronic, and Johnson & Johnson (J&J).Boston Scientific was the fastest to enter the Korean market, securing catheter certification for its FARAPULSE platform in April 2024 and generator approval in September.Analysts attribute this growth to the expanding market for electrophysiological procedures, driven by an increase in atrial fibrillation patients amid an aging population, with a recurring revenue model centered on related catheters and systems serving as the foundation for growth.In a Korea Health Industry Development Institute report on PFA, Professor Bo-young Joung of the Department of Cardiology at Severance Hospital stated, “PFA cuts procedure time by half compared with conventional methods and lowers complication risk, leading to high satisfaction among both physicians and patients. Currently, 35% of atrial fibrillation ablation procedures at Severance are performed using PFA, and this trend is expected to continue.”Given this, Boston Scientific Korea’s growth momentum is expected to strengthen further.Rezūm expansion and global M&A broaden business scopeAnother factor contributing to growth is the continued expansion of the Rezūm System, a medical device introduced in 2023 for benign prostatic hyperplasia, which has now surpassed 6,000 cumulative procedures in Korea.The Rezūm System received approval from the U.S. Food and Drug Administration (FDA) in 2015, obtained authorization from the Ministry of Food and Drug Safety in 2022, and was designated as a new health technology by the Ministry of Health and Welfare in 2023. Currently, Rezūm procedures are expanding their scope of application in clinical settings as a treatment option that can be considered even for patients unsuitable for medication or surgery.Regarding this, Boston Scientific Korea Country Manager Ae Ri Jung said, “Achieving 6,000 Rezūm procedures is a meaningful milestone demonstrating its establishment as a treatment option for BPH in Korea. We will continue contributing to expanding treatment options that improve patients’ quality of life.”As the portfolio expands, the company appears to be strengthening its field sales capabilities. Looking at the sales and administrative expenses, promotional expenses rose from KRW 6.3 billion in 2024 to KRW 7.1 billion in 2025.In particular, as Boston Scientific is pursuing mergers and acquisitions (M&A) on a global scale involving tens of trillions of won, its influence in the domestic medical market is expected to continue to grow in the future.The company acquired Axonics in 2024 to strengthen its urology portfolio, and in January, decided to acquire neurovascular treatment company Penumbra.In addition, it has also recently fully integrated Valencia Technologies, a urinary incontinence treatment company, rapidly expanding its portfolio.As the company expands its business scope to include new disease areas in addition to those that generate synergies with existing businesses, its business scale in the Korean market is also expected to grow.