- LOGIN

- MemberShip

- 2026-05-08 01:10:32

- Company

- Will the new prostate cancer drug Erleada be reimb in April?

- by Eo, Yun-Ho Mar 14, 2023 05:50am

- Whether the new prostate cancer drug ‘Erleada’ will be listed for reimbursement is gaining industry attention. The drug pricing negotiation period for Janssen Korea’s metastatic hormone-sensitive prostate cancer (mHSPC) treatment Erleada (apalutamide) with the National Health Insurance Service is about to expire this month (March). Erleada had passed deliberation by the NHIS Cancer Disease Deliberation Committee in February and then that of the Drug Reimbursement Evaluation Committee in December of the same year and has started the drug pricing negotiation process for its reimbursement earlier this year. If the pricing negotiations are completed within the set period, the agenda may be presented for review by the Health Insurance Policy Deliberation Committee in March. And if the agenda passes HIPDC review, the drug may be listed for reimbursement in April at the earliest. Erleada is an androgen receptor targeted agent (ARTA) and is a latecomer in the same class of drug as ‘Zytiga (abiraterone),’ or ‘Xtandi (enzalutamide).’ The drug’s efficacy was demonstrated through the Phase III TITAN trial that was conducted on 1,052 patients with mHSPC. Although 40% of the patients that were allocated to the placebo arm continued treatment with Erleada, the risk of death in the Erleada arm was 35% lower than that in the placebo arm. At 48 weeks, overall survival (OS) was 65% in the Erleada arm and 52% in the placebo arm. Also, when excluding the effect of patients who switched from the placebo to Erleada in the placebo arm, the risk of death in the Erleada arm was 48% lower than that of the placebo arm. According to data from the Cancer registration· Statistics Program, 16,815 patients in Korea were diagnosed with prostate cancer in 2020. Among men, prostate cancer is the third most common cancer in Korea, only headed by lung cancer with 19,657 patients and stomach cancer with 17,869 patients and followed by colorectal cancer, which has 16,485 patients. Moreover, among the five most common cancers in men (lung cancer, gastric cancer, prostate cancer, colorectal cancer, liver cancer), only the prevalence of prostate cancer has been increasing at an annual rate that exceeds 5%.

- Company

- Eylea makes sole lead in the ₩100B nAMD Tx market

- by Jung, Sae-Im Mar 13, 2023 05:53am

- (from the left) Eylea, Lucentis, Beovu The sole lead held by ‘Eylea’ in the domestic macular degeneration treatment market has been further solidified last year. Also, Novartis has been aggressively promoting sales of its recently launched new drug ‘Beovu.' With Novartis focusing its sales strategy on Beovu, sales of the company’s lesser priority, 'Lucentis,’ further declined last year. According to the market research institution IQVIA on the 11th, Korea’s macular degeneration treatment market grew by 14% YoY from KRW 111.1 billion the previous year and recorded KRW 126.3 billion last year.. Neovascular (Wet) Age-Related Macular Degeneration (nAMD) is considered one of the 3 major causes of blindness in the elderly aged 65 or older. The risk increases as one grows older. The growth of abnormal blood vessels (neovascular) results in the leakage of blood, lipid, or subretinal fluid, which damage the macula and lead to vision loss. Excluding ‘Avastin,’ which is used off-label, three treatments are available for nAMD in Korea – Bayer’s ‘Eylea (aflibercept),’ Novartis’s ‘Lucentis (ranibizumab)' and ‘Beovu (brolucizumab).’ Lucentis was the first to be approved in 2007, followed by Eylea in 2013. A decade later, Beovu was approved as a new drug. Also, another new drug, Roche’s ‘Vabysmo,’ was approved in January this year. Eylea made a new annual sales record of KRW 80.4 billion last year. This is a 14% YoY increase from KRW 70.5 billion in 2021. Eylea’s strength is that it allows patients to receive customized treatment by offering a broad dosing interval ranging from a minimum of 4 weeks to a maximum of 16 weeks. The drug contributed to the establishment of the treat-and-extend (T&E) regimen in nAMD treatment, where the patients’ dosing interval is regulated after monitoring the patients during the initial 3 months of treatment. Last year, the company introduced a pre-filled syringe formulation that reduces preparation time for drug administration by preparing the accurate dose for single administration in advance. The new formulation improved the convenience of the treatment process. However, sales of Lucentis, which was 2nd place in the market, have been decreasing for 2 consecutive years. Lucentis’s annual sales decreased by 16% from the KRW 35.1 billion to record KRW 29.4 billion last year. Lucentis’s sales have been decreasing continuously after peaking at KRW 37 billion in 2020. The change occurred when Novartis, its seller, received approval for its new nAMD treatment Beovu. Lucentis has been developed by Genentech and marketed by Roche and Novartis. In Korea, Lucentis is being sold by Novartis. Novartis developed its new drug and succeeded in receiving marketing approval for the drug in 2022. The decrease in Lucentis’s sales had been an expected result with Novartis focusing its capabilities on the sales of Beovu. Also, the entry of Lucentis’s biosimilars into the market upon Lucentis’s patent expiry heated up the competition this year. Chong Kun Dang and Samsung Bioepis started selling their Lucentis Biosimilars, ‘LucenBS,' and ‘Amelivu inj’ in January this year. With both drugs listed for reimbursement, Lucentis’s drug price had been reduced by 30% ex officio from February this year. Lucentis’s position as the original drug in the market is expected to weaken further as the companies that own Lucentis biosimilars have been competitively lowering drug prices to gain an advantage earlier in the market. Meanwhile, Novartis’s new drug Beovu’s sales exceeded KRW 10 billion last year. Last year, Beovu’s sales increased 205% YoY from the KRW 5.4 billion in the previous year to record KRW 16.5 billion. Unlike other existing treatments that have dosing intervals of 4-8 weeks, Beovu has a dosing interval of up to 12 weeks (3 months). This was evaluated to have improved patient compliance by reducing the difficulties of patients that had to receive injections into the eye. The low compliance in patients with nAMD had been pointed to as a major issue that reduces the actual treatment effect of the nAMD treatments. Beovu demonstrated its non-inferiority with Eylea with its 12-week administration through a head-to-head trial. The therapeutic effect lasted until week 96. Also, the Beovu-treated group showed superior improvement in intra-retinal fluid and sub-retinal fluid compared to the Eylea-treated group The reason Beovu produces a similar effect despite the longer dosing interval is due to its molecular characteristics. Beovu’s single-chain antibody fragment (ScFv) is engineered to deliver a higher concentration of molecules compared to other treatments with multiple chains. However, HCPs have been showing divided opinions on its use due to its side effect of retinal vasculitis, which is unseen in other existing treatments. In particular, the introduction of Vabysmo, the first bispecific antibody introduced to the field of ophthalmic diseases, is expected to somewhat dilute Beovu’s strengths of 'high efficacy and convenience.’ Vabysmo is the first bispecific antibody that targets both the VEGF which is commonly targeted by existing ocular disease treatments as well as Ang-2 that is considered to be the cause of retinal disease to block both pathways. In particular, it has improved convenience in administration over other existing treatments with a dosing interval of up to 16 weeks (4 months). If listed for reimbursement, Vabysmo is expected to start a full-fledged competition with Beovu.

- Company

- Pharmaceutical companies are fiercely competing to develop

- by Kim, Jin-Gu Mar 13, 2023 05:53am

- In the hyperlipidemia combination drug market of 'statin + ezetimibe', competition to develop a two-drug combination using 'low-dose statin' is intensifying. According to the pharmaceutical industry on the 11th, Yuhan Corporation is developing a combination drug for hyperlipidemia with Ezetimibe added to Atorvastatin 5mg through its subsidiary Addpharma. Yuhan already has three products, including Atovamibe, a two-component complex. The dose of Ezetimibe is the same at 10 mg, and only the doses of Atorvastatin are different at 10 mg, 20 mg, and 40 mg. Yuhan Corporation's plan is to add a combination drug based on the 5mg dose of Atorvastatin. Rosuzet 10/2.5mg, a low-dose hyperlipidemia drug from Hanmi Pharmaceutical According to the original developer, Addpharma, the development of the corresponding dose product is currently in the final stage, and it is expected that it will be possible to apply for product approval as early as this month. If the item is approved by the Ministry of Food and Drug Safety, it will be the first product for hyperlipidemia combined with low-dose atorvastatin. In addition to Addpharma, several companies are said to be developing complex drugs with the same combination of ingredients and doses. This is the background to the prospect that competition in the market for the variety of Atorvastatin 5mg and Ezetimibe will intensify in the future. Hanmi Pharmaceutical opened the door to developing a combination drug for hyperlipidemia based on low-dose statins. In September 2021, Hanmi Pharmaceutical obtained permission for 'Rosuzet 10/2.5mg', in which Ezetimibe was added to Rosuvastatin 2.5mg. It is known that the low-dose product is rapidly increasing prescription performance after the benefit was launched in October of that year. According to UBIST, a pharmaceutical market research institute, the outpatient prescription amount of Rosuzet increased by 14% from the previous year to 140.3 billion won last year. The pharmaceutical industry believes that the addition of low-dose products contributed to the expansion of Rosuzet's overall prescription record. Recently, it is said that the monthly prescription amount has expanded to more than 1 billion won. As low-dose Rosuzet gained market acceptance, other companies jumped into developing low-dose Rosuvastatin-based combinations. Daewoong Pharmaceutical received approval for Crezet 10/2.5mg with the same ingredient and dose combination as Rosuzet in August of last year. Since February of this year, Yuhan Corporation's Rosuvamibe, HK inno.N Rovazet, and GC Pharma Daviduo have also added low-dose Rosuvastatin-based complexes to their product lineups. An official from the pharmaceutical industry said, “The core dose of Rosuvastatin was 5 mg, and Hanmi Pharmaceutical succeeded in increasing the prescription performance of Rosuzet by releasing a low-dose product that halved the dose.” There is a possibility of market success because the product is half the existing core dose (10 mg).”

- Company

- Gastric cancer is the first immuno-oncology option available

- by Eo, Yun-Ho Mar 13, 2023 05:53am

- In the field of gastric cancer, attention is paid to whether the first immuno-oncology drug insurance benefit registration can be achieved. As a result of the coverage, it is possible to propose the HIRA in April for Opdivo, an immune anticancer drug with PD-1 inhibitory mechanism, from Ono Korea Pharmaceuticals and Korea BMS Pharmaceuticals. In June 2021, Opdivo added an indication for 'combination therapy with fluoropyrimidine-based and platinum-based chemotherapy as the first-line treatment for advanced or metastatic gastric adenocarcinoma, gastroesophageal junction adenocarcinoma, or esophageal adenocarcinoma' in Korea. It is the first and only approved immune anti-cancer drug in Korea for first-line gastric cancer treatment. This drug failed to pass the HIRA committee in February of last year and submitted a re-application, and passed the cancer disease review committee in June of the same year. If it is presented to the committee in April and passed, it is expected that the first half of the year will be possible at the earliest. Opdivo was also recognized for its benefit adequacy in the UK at the end of last year. The National Institute of Health and Clinical Excellence recently recommended Opdivo for use in chemotherapy-naive patients with PD-L1 expression, HER-2 negative, advanced metastatic gastric cancer or gastroesophageal junction cancer, and esophageal adenocarcinoma. Gastric cancer is currently the second largest cancer after lung cancer, and the need to expand the reimbursement of immuno-anticancer drugs is on the rise. Gastric cancer is a typical cancer type that ranks first in the prevalence of cancer and the fourth leading cause of cancer death in Korea. If detected early, the survival rate is good, but when distant metastasis progresses, the 5-year relative survival rate drops sharply to 5.9%. In particular, HER2-negative gastric cancer patients, who account for 90% of advanced gastric cancer patients, have been receiving chemotherapy as a standard treatment since there has been no newly approved new drug in the first-line treatment for the past 10 years. Opdivo could be an alternative for these patients.

- Company

- GC Pharma begins develop of mRNA flu vaccine candidates

- by Hwang, Jin-joon Mar 10, 2023 05:50am

- GC Pharma researcher is conducting drug research. (Photo by GC Pharma)Invested in mRNA pilot production facilities in Hwasun Vaccine Plant in Jeollanam-do. GC Pharma announced on the 9th that it will apply Acuitas Therapeutics' Lipid Nano Particle (LNP) technology to develop mRNA flu vaccine candidates in earnest. GC Pharma signed an LNP-related Development and Option Agreement with Acuitas in Canada in April of last year. Through the study, the possibility of developing an mRNA flu vaccine was confirmed. We recently exercised our non-exclusive licensing agreement option for the LNP. LNPs safely transport nanoparticles into cells in the body to help mRNA function. It is a key technology required for mRNA-based drug development. The LNP technology owned by Acuitas, a company specializing in the development of LNP delivery systems, was also applied to Pfizer's COVID-19 vaccine COMIRNATY. GC Pharma plans to conduct a phase 1 clinical trial of its mRNA vaccine candidate in 2024. GC Pharma also started investing in mRNA production facilities. It decided to invest in mRNA trial production facilities at its Hwasun plant in Jeollanam-do, which produces the existing flu vaccine.

- Company

- Myelofibrosis New Drug Inrebic

- by Eo, Yun-Ho Mar 10, 2023 05:50am

- Inrebic, a myelofibrosis treatment option born 10 years after Jakavi, is accelerating its steps toward insurance coverage. As a result of the coverage, BMS Pharmaceutical's myelofibrosis treatment Inrebic is in the process of drug price negotiations with the NHIS. Depending on the negotiation date, it is expected that it will be possible to determine whether or not to register in April. Inrebic was approved in Korea in April of last year for the treatment of splenomegaly or symptoms related to primary myelofibrosis, polycythemia vera, and myelofibrosis after essential thrombocythemia in adult patients previously treated with Jakavi. An application for reimbursement was submitted, but in June of last year, it failed to pass the HIRA, after re-application, it passed both the Cancer Disease Review Committee and the Pharmaceutical Reimbursement Evaluation Committee last month. This drug is a JAK-2 inhibitor and is expected to be different from Jakavi, a JAK1/2 inhibitor. Inrebic is the first to obtain approval for an oral once-a-day drug that greatly reduces the burden of spleen volume and symptoms in patients with myelofibrosis who have not had a history of treatment. Myelofibrosis is a rare blood cancer that affects the bone marrow and interferes with the body's normal production of blood cells. Patients suffer from symptoms such as an enlarged spleen, fatigue, itching, weight loss, night sweats, fever, and bone pain, which affect their quality of life. experience symptoms. Jakavi was the only JAK inhibitor approved for the treatment of myelofibrosis, and there was no alternative for patients who failed treatment. Inrevic is a treatment that appeared 10 years after Jakavi in the myelofibrosis market, where there was no second-line treatment option. Inrebic is currently covered through the Cancer Drug Fund in the UK. In 2021, NICE refused to apply Inrebic for NHS coverage. However, CDF recommends the use of Inrebic within its oncology fund for the treatment of splenomegaly or other symptoms associated with the disease in patients with myelofibrosis who have previously been treated with Jakavi.

- Company

- Enbrel's share is 44% and Herceptin's share is 37%

- by Kim, Jin-Gu Mar 10, 2023 05:50am

- Mabthera, Avastin, and Humira similars also saw a sharp rise in market share new product addition effect. The share of biosimilar products in the domestic market is rapidly expanding. Enbrel biosimilars Etanercept increased its market share from 12% in 2018 to 44% last year. Herceptin similars also expanded from 9% to 37% during the same period. ◆Eucept and Remaloce, Enbrel similar, had a 44% market share with sales of 8.1 billion won last year According to IQVIA, a pharmaceutical market research institute, on the 10th, the market for Etanercept ingredient treatment last year was 18.2 billion won. Pfizer Enbrel, the original product, recorded 10.1 billion won and Enbrel biosimilar 8.1 billion won, respectively. In terms of market share, original drugs accounted for 56% and biosimilars 44%. The market share of biosimilars has risen significantly over the past four years. In 2018, Enbrel's biosimilar market share was only 12%, but it increased by 32%p in 4 years, greatly narrowing the gap with the original. LG Chem's Eucept and Samsung Bioepis' Remaloce have been released as Enbrel biosimilars. Last year's sales were 4.1 billion won for Eucept and 4 billion won for Remaloce. Until now, biosimilars have been evaluated as not impacting the domestic market, unlike Europe and the United States. It is analyzed that recently, biosimilar products are gradually increasing their influence in Korea. It is analyzed that new products have been steadily released, centered on Samsung Bioepis and Celltrion, and the preference for similar products has gradually increased in the prescription field. ◆Herceptin-similar market share 9% → 37%/ Avastin similar achieved 21% in 1 year Other biosimilars have also significantly increased their market share recently. In the case of the trastuzumab market, the share of Herceptin biosimilars increased by 28%p in 4 years from 9% in 2018 to 37% last year. Celltrion Herzuma and Samsung Bioepis Samfenet were released as Herceptin biosimilars. Last year, sales were 29 billion won for Herzuma and 5.6 billion won for Samfenet. Herzuma's sales increased 3.7 times in 4 years from 7.7 billion won in 2018 to last year. Samfenet increased 2.5 times in 3 years from 2.2 billion won in 2019. The original Herceptin sales decreased by 25% from 80 billion won in 2018 to 60 billion won last year. Original's market share declined from 91% to 63%. Avastin biosimilars are also rapidly expanding their market share. Samsung Bioepis released the Avastin biosimilar Onbevezy in the fourth quarter of 2021. Onbevezy, which recorded sales of 500 million won in the first year of its release, saw its sales skyrocket to 20.5 billion won last year. As sales soared, Onbevezy's Bevacizumab market share quickly expanded to 21%. Here, Celltrion Vegzelma, Alvogen Korea Alymsys, and Pfizer Korea Pharmaceutical ZIRABEV are aiming to enter the market. If these products are added in earnest, the share of biosimilars in the Avastin market is expected to rise further. Mabthera biosimilars' share in the rituximab market increased from 8% in 2018 to 25% last year. Currently, Celltrion's Truxima is sold alone. Humira biosimilars recorded a 9% market share last year. Samsung Bioepis released Adalloce in the third quarter of 2021, and Celltrion released Yuflyma in the third quarter of last year. Sales last year were 7.6 billion won for Adaloch and 500 million won for Yuflyma. Remicade biosimilars recorded a 38% market share last year. Celltrion Remsima posted 29.3 billion won in sales last year, and Samsung Bioepis Remaloce posted 4.9 billion won in sales. The original Remicade's sales are 55.5 billion won.

- Company

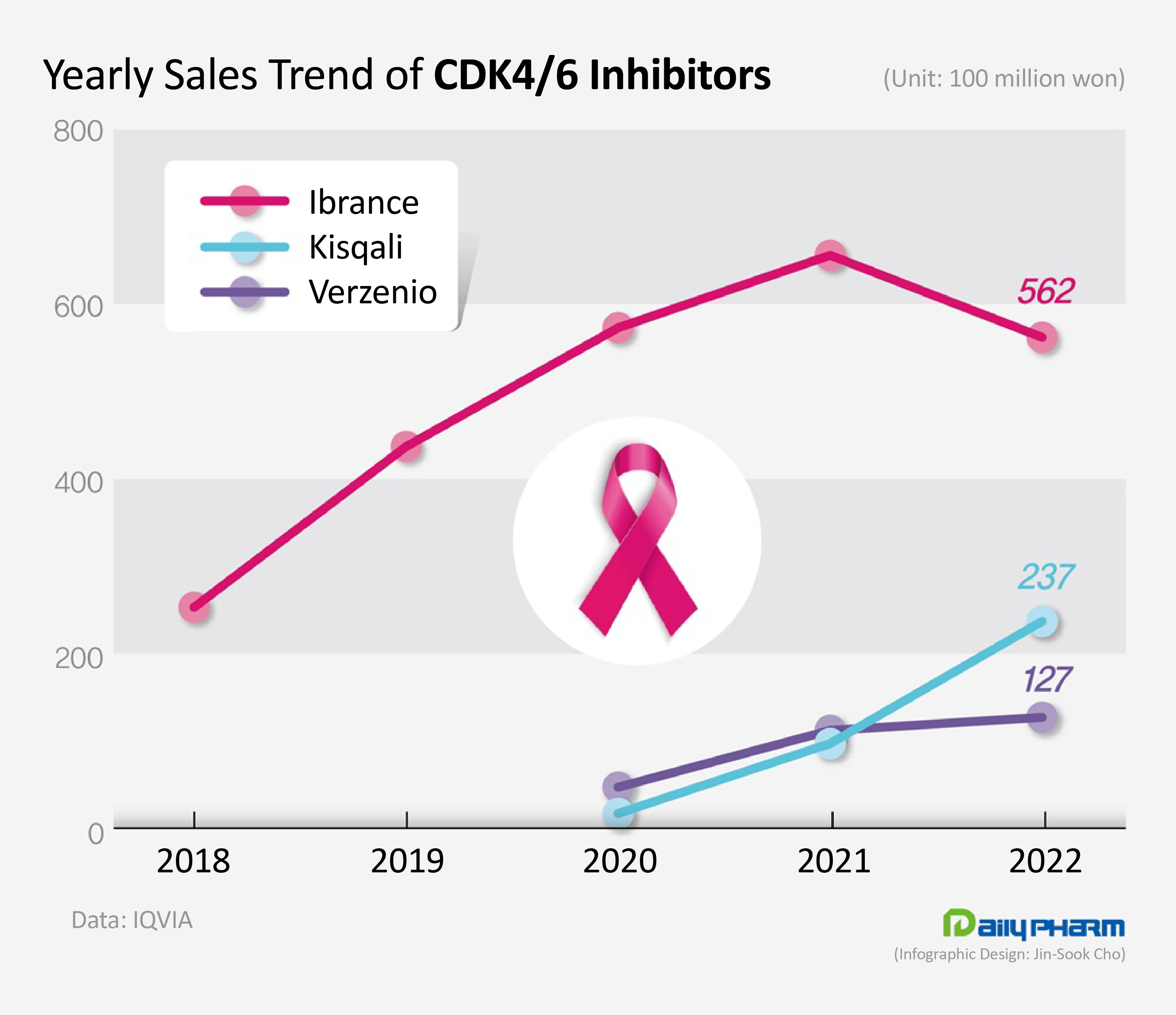

- Sales of Kisqali surge, Ibrance decline

- by Jung, Sae-Im Mar 09, 2023 06:00am

- The market for cyclin-dependent kinases (CDK) 4/6 inhibitors that are used to treat metastatic breast cancer have undergone drastic changes last year. Sales of Ibrance, which used to dominate the market, had faltered, while the latecomer Kisqali rapidly expanded its share in the market . According to the market research institution IQVIA on the 8th, the domestic market for CDK 4/6 inhibitors increased 7.1% YoY from KRW 86.5 billion in the previous year to ₩92.6 billion last year. CDK, cyclin-dependent kinases, control cell division and growth. CDK 4/6 inhibitors selectively inhibit CDK 4/6 to suppress the proliferation of cancer cells. These drugs are mainly used to treat hormone receptor (HR)-positive or human epidermal growth factor receptor 2 (HER2)-negative advanced or metastatic breast cancer, which accounts for 60% of all breast cancers. Since the introduction of the first-in-class CDK 4/6 inhibitor, Pfizer’s Ibrance (palbociclib), Novartis’s Kisqali (ribociclib), and Lilly’s Verzenio (abemaciclib) are also available in the market. Ibrance, which overtook the market as the 'first-in-class' drug, experienced its first decline in sales last year. Ibrance’s sales fell 14.3% YoY from the KRW 65.6 billion in the previous year to record sales of KRW 56.2 billion last year. The drug, which had shown repeated growth since its launch, faced a decline in sales for the first time in six years. The first CDK 4/6 inhibitor Ibrance was developed by Pfizer and released in Q4 2016 in Korea. The drug offered a new treatment option for patients with HR+/HER2- metastatic breast cancer that were left to use chemotherapy for their disease that cannot be controlled with hormone therapies like aromatase inhibitors. Upon its release, Ibrance was received with high expectations in the market, being the first drug to demonstrate a PFS of over 2 years. Ibrance’s sales rose sharply from KRW 6.6. billion in 2017 to KRW 25.3 billion in 2018, KRW 43.7 billion in 2019, and then KRW 57.3 billion in 2020. The sales decline started with the introduction of its latecomers. Kisqali and Verzenio entered the market in 2020 and started expanding their presence ever since. Among the latecomers, Kisqali has been showing marked growth. Kisqali’s sales rose 143.6% YoY from the KRW 9.7 billion earned in the previous year to record KRW 23.7 billion last year. Although it had the lowest share of the market with annual sales of less than KRW 10 billion until 2021, its sales had risen to the KRW 20 billion range last year and exceeded Verzenio’s sales. The fact Kisqali is the only treatment option among CDK4/6 inhibitors that can be used in premenopausal breast cancer patients seems to have contributed to its rapid growth. Ibrance and Verzenio are only indicated for the treatment of postmenopausal women with metastatic breast cancer. However, Kisqali demonstrated its effect in premenopausal patients in clinical trials. Unlike in the West where premenopausal patients account for less than 30% of the patient population, these women account for 55% of the patient population in Korea, which explains the increased use of Kisqali. However, sales of Verzenio, which have risen sharply in 2021, had also slowed down somewhat. Verzenio’s sales increased 13.7% YoY from the KRW 11.2 billion in the previous year to KRW 12.7 billion last year. Verzenio is seeking to expand its market base this year after it had become the only CDK4/6 inhibitor allowed for use in early breast cancer. The Ministry of Food and Drug Safety additionally approved Vezenio as an adjuvant treatment for patients with HR+ /HER2- type lymph node-positive, early breast cancer at high risk of recurrence. This is the first time a new drug was approved for early breast cancer after the approval of aromatase inhibitors.

- Company

- Childhood dementia Tx Xenpozyme to soon land in KOR

- by Eo, Yun-Ho Mar 09, 2023 06:00am

- The first childhood dementia treatment is expected to be commercialized in Korea soon. According to industry sources, the Ministry of Food and Drug Safety is conducting the final review to approve Sanofi Genzyme’s treatment for acid sphingomyelinase deficiency (ASMD)m ‘Xenpozyme (olipudase alfa).’ Starting with Japan in March, the drug was also approved in Europe in July and by the US FDA in August and received Breakthrough Therapy designation in the countries. The drug received final review in July and September in Europe and the US, respectively. The efficacy of Xenpozyme, the only existing ASMD treatment, was identified through the ASCEND and ASCEND-Peds trials. The ASCEND trial evaluated the efficacy and safety of Xenpozyme in 36 adult patients with ASMD type A/B or type B. The patients were randomized to receive Xenpozyme or a placebo for 52 weeks (primary analysis). At Week 52, Xenpozyme improved pulmonary function from baseline by 22% in the predicted diffusing capacity of carbon monoxide (DLco). Compared with the 3% improvement shown in the placebo group, the difference between the two treatment arms of 19% was statistically significant. Also, at Week 52, patients treated with Xenpozyme had a mean reduction in spleen volume by 39.5% compared with the 0.5% increase in the placebo group. All patients that were treated with Xenpozyme showed an improvement in one or two primary endpoints. The single-arm ASCEND-Peds trial studied 20 pediatric patients younger than 12 years of age with ASMD type A/B or type B. The primary objective of the trial was to evaluate the safety and tolerability of Xenpozyme for 64 weeks, and the explored efficacy endpoints of progressive lung disease, spleen, and liver enlargement, and platelet count were also explored in the trial. The nine patients who could take the test for DLco in the trial showed a 33% improvement in diffusing capacity after 1 year. The patients also showed a mean reduction in spleen volume of 49%. Meanwhile, ASMD is caused by the lack of an enzyme needed to break down a complex lipid, called sphingomyelin, which accumulates in the liver, spleen, lung, and brain. Patients with ASMD experience enlarged abdomens at 3 to 6 months of birth. The most severely affected patients have profound neurologic symptoms and rarely survive beyond two to three years of age.

- Company

- Hemlibra is also effective for mild and secondary hemophilia

- by Kim, Jin-Gu Mar 09, 2023 06:00am

- JW Pharma announced on the 6th that Phase III clinical trials that proved the effects and safety of patients with type hemophilia have been published in the online edition of the Lancet Hematology 2023, an international journal. Hemlibra is a type A hemophilia disease caused by the deficiency of factor XIII. It is the only anti-antibody patient and non-antibody patient with resistance to the existing therapeutic agent (8-factor formulations), and the prevention effect persists with subcutaneous injections for up to 4 weeks. Type A hemophilia is divided into mildness (more than 5% to less than 5% to less than 40%), moderate (1% or more to 5% or less), and severe (less than 1%) according to the figures of factor XIII activation. Hemlibra has been licensed in Korea for severe A-type hemophilia prevention therapy. 18 professors, including Claude Bernard Lyon 1 University, conducted about 55 weeks of clinical trials for 72 patients with mild and secondary A-type hemophilia in 22 institutions, including Europe, North America, and South Africa. The researchers administered to patients once a week for the first four weeks of Hemlibra, and then selected once a week or once ▲ 4 weeks once a week to evaluate the bleeding volume and thrombosis adverse events. Annual Bleed Rate, which was 10.1 times, decreased by 0.9 times after hembra administration. Among them, joint bleeding and natural bleeding ABRs, which required treatment, were 0.2 times. 21 mild patients have decreased from 20.2 times before Hemlibra administration, and 2.4 times after administration, while moderate patients decreased from 6.0 to 2.2 times. The ABR of the patient group, which had been treated with the existing coagulation factor treatment as a preventive therapy, was improved from 8.0 to 2.4 times after clinical 12.2 times before clinical trials and bleeding groups. Eight patients were not bleeding during the clinic. In terms of safety, 15 patients had minor side effects related to the injection site, but no death or thrombectomy microvascular disease occurred. Based on these clinical results, Hemlibra was approved by the European Union (EU) as a preventive treatment for patients with non-antibody aid type hemophilia. An official of JW Pharma said, "This clinical trial indicates that Hemlibra is effective in preventing bleeding for patients with mild and secondary A-type hemophilia." said. Hemlibra was developed by Japan's Chugai Pharmaceutical, a subsidiary of Global Pharm Roche. JW Sino -Pharmaceuticals secured domestic development and copyrights of Hemlibra in 2017 and launched it as a treatment for severe A-type hemophilia in 2020.