- LOGIN

- MemberShip

- 2026-05-02 18:23:09

- Company

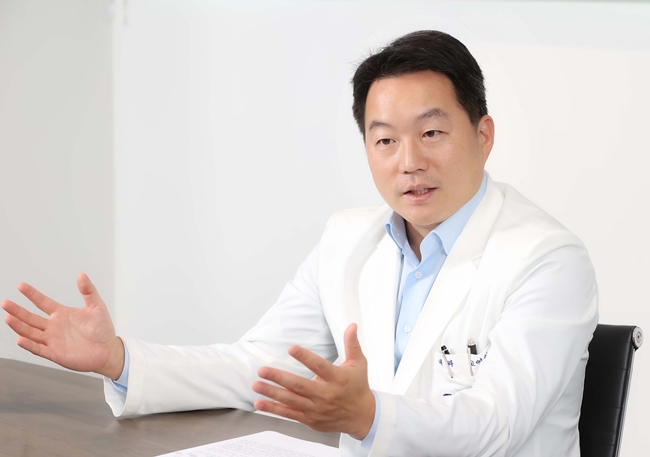

- "Multiple myeloma dynamics require changes to reimb strategy

- by Whang, byung-woo Oct 22, 2024 05:51am

- Youngil Koh, Professor of the Department of Hemato-Oncology at Seoul National University Hospital "Multiple myeloma is a cancer type that has a great ripple effect depending on new drugs provided in a certain environment. Reimbursement of multiple myeloma treatment requires discussion following a thorough evaluation of the impact of the treatment depending on the treatment environment." Multiple myeloma is one of the cancer types with increased treatment options following new drug entries. There are concerns about extending the relapse period and progression-free survival (PFS) as the number of treatments increases due to relapses. However, the discussion for reimbursement is hindered by cost issues. Youngil Koh, Professor of the Department of Hemato-Oncology at Seoul National University Hospital, emphasizes the importance of discussing appropriate disease-specific environments. According to Koh, the development of new drugs for blood cancers is active because of disease characteristics. Because cancer cells tend to exist in the blood and it is easy to obtain samples, the research is relatively simple. Understanding of blood cancer yields significant results compared to solid cancers. "Almost all new drugs begin from blood cancers, including TKI, therapeutic antibody, bispecific antibody, and ADC, and expand to solid cancers. Bispecific antibodies and ADCs are used as the standard treatment for blood cancers and expand their indications to solid cancers," Koh said. In South Korea, a bispecific antibody treatment, Tecvayli (teclistamab), is available for treating multiple myeloma. This drug was approved in July. The use of Tecvayli is limited because it is not reimbursed, but the expansion of market presence is expected following the announcement of long-term follow-up research results of the drug's clinical trial, MajesTEC-1, at the American Society of Clinical Oncology (ASCO 2024) meeting. The results of evaluating the efficacy of Tecvayli in 165 study participants at 30.4 months interim follow-up showed that Tecvayli reduced tumor sizes by 63% (overall response rate, ORR) in patients who had failed or were non-responsive to third-line treatments or higher. 46.1% of the patients reached complete remission (CR). The study confirmed consistent, long-term clinical effectiveness and positive safety profile. "The 30-month follow-up outcome did not differ from the data presented in 2022; therefore, it is significant that we have confirmed the anticipated outcome," Koh said. "Specifically, 4 out of 10 patients showed great responses and maintained response over two years." "We have observed that the real effects observed in 30-50 patients administered with the drug at the Seoul National University Hospital did not differ greatly from the research," added Koh. "1/3 of the patients benefited from the treatment, and close to half experienced great responses." In conclusion, Koh says that the result should be highly regarded because Tecvayli's long-term follow-up data demonstrated that patients showed a significantly long response period after almost two-years of treatment. Will Tecvayli, demonstrating its long-term effects, be adminstered earlier in the treatment course? Based on the assumption that there are no differing opinions about the effect of Tecvayli, the question is 'when' to use the drug. There are concerns about using the good drug first or last, regardless of disease. However, multiple myeloma requires a more careful approach because the treatment order is particularly important. Koh says it is difficult to determine at this point, but Tecvayli is likely to be placed earlier in order since the data supporting its use of Tecvayli in earlier treatment course are now available. "Tecvayli is the only bispecific antibody to be used for the treatment of multiple myeloma in South Korea and it targets BCMA, which the conventional treatments haven't targeted," Koh said. "Based on the clinical data of Tecvayli used in combination with already effective treatments that are currently used, Tecvayli is likely to be employed earlier in the treatment and will be able to extend overall survival," Koh said. However, Koh assessed that it is too early to mention whether bispecific antibody, known as the next-generation treatment, or CAR-T therapy should be placed earlier. "The positions of bispecific antibody and CAR-T for treating multiple myeloma have not been established yet. We now know that two treatments successfully treat multiple myeloma, but it is early to determine which one is superior. Upcoming clinical data will determine their positions," Koh emphasized. "Multiple myeloma is highly dynamic…changes to reimbursement strategy should be considered" Besides the Tecvayli effect, the dilemma for new drugs is the cost. Patient burden increases when high-cost drugs are not covered by reimbursement. Since multiple myeloma treatment tends to use 2-3 treatments in combination, the government is hesitant to opening the door to reimbursement. Regarding this issue, Koh advises that rather than simply comparing the cost of the drug, a reimbursement strategy reflecting the characteristics of multiple myeloma should be discussed. "The dynamic of treatments for multiple myeloma is changing due to new drugs, and the disease is greatly influenced by the type of new drugs and the type of reimbursement. We need to discuss reimbursement after anticipating the potential impact of reimbursement on overall treatment outcomes," Koh explained. "The landscape of multiple myeloma is diverse and constantly changing; therefore, instead of simply comparing costs, the government can strategize better reimbursement plan taking into account various outcomes," Koh said. Koh stated that we need to discuss patient access to clinical trials while reimbursement for new drugs is limited. "New drugs are being developed faster than the reimbursement process. It is inevitable that patients cannot benefit from new drugs because reimbursement cannot cover all," Koh said. "In other words, drugs are available at clinical stages, so we could discuss increasing patient access to new drugs."

- Company

- Will combination therapies for cancer be reimbursed in KOR?

- by Whang, byung-woo Oct 21, 2024 05:49am

- As the government has begun to prepare the principles for the reimbursement review of combination therapies that use new anticancer drugs, attention is being paid to whether the discussion will progress further. According to industry sources, the Health Insurance Review and Assessment Service recently held a Cancer Disease Deliberation Committee meeting and decided to prepare deliberation principles to discuss whether to approve benefits for major combination therapies. The decision is in line with the growing calls for a change in the reimbursement paradigm for prescribing anticancer drugs based on accumulated evidence on ‘combination therapies’ between treatments from various clinical studies. Recently, multinational pharmaceutical companies have been seeking the reimbursement of combination therapies using new anticancer drugs, calling for an institutionalized process. When considering reimbursement for combinations of non-reimbursed new drugs and reimbursed chemotherapy drugs, the industry has suggested that discussions on previously reimbursed drugs should be reserved and only the non-reimbursed drugs should be discussed. A case in point is AstraZeneca's immuno-oncology drug Imfinzi (durvalumab), the reimbursement of which had been discussed for biliary tract cancer last year. At the time, CDDC only approved gemcitabine and cisplatin in combination with chemotherapy (the GemCis regimen) for first-line treatment of biliary tract cancer, while leaving Imfinzi non-reimbursed. The government will discuss setting a deliberation principle where a drug, which is already reimbursed, is used with a non-reimbursed new drug as part of combination therapy and should continue to be reimbursed without further discussions. This can be observed in the results of the 7th CDDC Review, which reviewed the combination of ‘endocrine therapy’ and ‘Verzenio (abemaciclib)’ for the treatment of early breast cancer. The outcome of the deliberations was to keep the previously reimbursed adjuvant endocrine therapy as is and make the newly added Verzenio available on a ‘100% coinsurance’ basis, reducing the cost burden on the patients. In other words, it means that the process will be simplified by allowing the reimbursement of existing treatments within the combination to be recognized. However, these principles are not automatically applicable to all new combination therapies, and as it leaves the existing framework in place, it is far from the improvements to the new drug approval approaches the industry had hoped for. Nevertheless, it is positive as it has opened the door to further discussions. There are also expectations that such discussions will lead to solutions for ‘new drug+new drug’ combination therapies. A pharmaceutical industry official said, “It is still a drug-by-drug approach, so it's not a one-size-fits-all approach, but it's positive that the discussions have been officially made. We understand that KRPIA and others are also having discussions on what kind of processes will be required for the reimbursement of new drugs for combination therapies in the future,’ “With the number of combination therapy cases increasing, there is currently no set process for how applications should be submitted for listing and how they should be reviewed. We are looking forward to the various approaches that may be developed through discussions as individual cases have come to light.”

- Company

- Therapeutic device 'improves OS for lung cancer patients'

- by Son, Hyung Min Oct 21, 2024 05:48am

- The first therapeutic device has been approved for use in non-small cell lung cancer (NSCLC). Novocure's therapeutic device, in combination with an NSCLC medication, demonstrated to improve patients' overall survival and won the approval of the U.S. regulatory authority. In South Korea, Nu Eyne is researching the potential of oncology therapeutic devices through clinical studies. According to industry sources on October 19th, the U.S. Food and Drug Administration (FDA) granted approval for Novocure's Optune Lua for the treatment of metastatic non-small cell lung cancer (NSCLC). Optune Lua is approved for use in combination with PD-1/PD-L1 immunotherapy for cancer or docetaxel. Optune Lua is a device that delivers 'Tumor Treating Fields (TTFields),' which exert physical forces on the electrically charged components of dividing cancer cells, resulting in cell death. Novocure says that TTFields do not affect healthy cells because they have different properties (including division characteristics, morphology, and electrical properties). The basis of approval was the Phase 3 LUNAR study. The clinical trial involved 301 patients with NSCLC who had failed during or after platinum-based chemotherapy. The patients were randomly assigned in a 1:1 ratio to the group receiving Optune Lua plus a PD-1/PD-L1 inhibitor or docetaxel or to the single-treatment group receiving a PD-1/PD-L1 inhibitor or docetaxel. Clinical results showed Optune Lua combination therapy recorded a median overall survival (OS) of 13.2 months, set as the primary endpoint. This was 3 months longer than 9.9 months in the control group. Patients randomly administered Optune Lua plus immunotherapy had a median OS of 19.0 months, and patients administered a PD-1/PD-L1 inhibitor alone had a median OS of 10.8 months. The Optune Lua combination therapy group had an OS extension of over 8 months compared to patients treated with immunotherapy alone. Patients randomly administered Optune Lua plus docetaxel had a median OS of 11.1 months, whereas patients treated with docetaxel had a median OS of 8.9 months. However, this figure did not show a statistically significant difference. Device-related adverse events (AE) occurred in 63.1% of patients treated with Optune Lua combination therapy. Most cases were Grade 1-2 and only 4% (6 patients) experienced Grade 3 skin toxicity and discontinued treatment. Optune Lua did not show Grade 4-5 toxicity, and no deaths occurred. Therapeutic device is being developed in South Korea…Nu Eyne challenges the field A Korean company, Nu Eyne, has confirmed the effects of immunotherapy and is conducting therapeutic device development. To confirm treatment effects on cancer, Nu Eyne conducted a cell-based clinical study to compare the stimulated group to the non-stimulated group of cultured cells after 48 hours of electrical stimulation. The results showed that the electrically stimulated group had an up to 80% reduction in tumor size. Nu Eyne's technology for its oncology therapeutic device has been developed to deliver a high-intensity electrical field that responds particularly to cancer cells, thereby inducing cell death. The technology is known to have a low risk of causing side effects on surrounding organs. Nu Eyne is developing advanced systems and materials to maximize oncology therapeutic effects. Using its technology, Nu Eyne aims to develop therapeutic devices to secure indications for treating lung cancer and bone metastatic cancer. Nu Eyne aims to complete the development of a clinical therapeutic device prototype in the second half of 2026. After that, the company plans to conduct clinical trials to secure the FDA regulatory approval.

- Company

- Oxlumo receives orphan drug designation in Korea

- by Eo, Yun-Ho Oct 21, 2024 05:48am

- The primary hyperoxaluria treatment Oxlumo received orphan drug designation in Korea. The Ministry of Food and Drug Safety (MFDS) recently announced the designation through an orphan drug designation notice. Oxlumo (lumasiran) was also recently designated a Global Innovative products on Fast Track (GIFT) by the MFDS. The drug is an RNAi therapeutic for primary hyperoxaluria (PH1), a rare kidney disease that was approved by the US Food and Drug Administration (FDA) and the European Medicines Agency (EMA) in 2020. RNAi is recognized as a next-generation gene therapy that has the advantage of providing specific access to disease-causing human genes. PH1 is a rare disease caused by excessive production of oxalate in the liver. Symptoms include the deposition of oxalate crystals or potassium oxalate crystals in the kidneys and urinary tract. As the disease progresses, kidney damage occurs and dialysis is required. Eventually, a liver or kidney transplant is required to cure the disease. The option to treat PH1 with a therapeutic agent became available with the approval of Oxlumo in 2020. Oxlumo is an RNAi therapy that targets hydroxy acid oxidase 1 (HAO1), which encodes glycolate oxidase (GO), the enzyme that produces oxalate. The mechanism of action reduces oxalate by inhibiting HAO1, which reduces GO production. Oxlumo’s efficacy was confirmed through a Phase III clinical trial in 39 PH1 patients aged 6 years and older. Oxlumo reduced oxalate levels in the urine by 65.4% compared to the placebo group. In addition, 84% of patients treated with Oxlumo had urinary oxalate levels near normal. 52% achieved urinary oxalate levels within the normal range.

- Company

- RNAi therapeutic 'Givlaari' receives the ODD in KOR

- by Eo, Yun-Ho Oct 21, 2024 05:48am

- Product photo of Givlaari (givosiran) RNAi therapeutic 'Givlaari' has been designated as an orphan drug following its designation as the GIFT. The Ministry of Food and Drug Safety (MFDS) recently announced this through the posting of the Orphan Drug Designation (ODD). Givlaari (givosiran) had previously been designated as the 'Global Innovative products on Fast Track (GIFT)' by the MFDS. This drug won U.S. FDA approval in 2019 and also received the accelerated approval from Europe's EMA. Givlaari is a subcutaneous injection that targets the enzyme aminolevulinic acid synthase 1 (ALAS1) for the treatment of acute hepatic porphyria (AHP) in adults and adolescents aged 12 years and older. AHP is caused by a genetic deficiency due to the depletion of the enzyme needed for heme biosynthesis in the liver. It is a rare genetic disorder with abnormal accumulation of porphyrins in the body. Patients with AHP experience debilitating symptoms, such as severe abdominal pain, vomiting, and seizures, and chronic pain. The efficacy of Givlaari has been demonstrated through the Phase 3 ENVISION clinical trial. Givosiran was shown to reduce the occurrence of annual porphyria-associated seizures by 74% compared to the placebo. The research outcome was published in The New England Journal of Medicine (NEJM) on June 11th, 2020. During the six months of treatment, the percentage of patients who had not experienced porphyria-associated seizures was 50% for the givosiran-treatment group and 16.3% for the placebo group.

- Company

- Bladder cancer drug Balversa offers new treatment option

- by Whang, byung-woo Oct 18, 2024 05:49am

- The introduction of the targeted therapy Balversa (erdafitinib) in urothelial carcinoma has attracted attention for its potential to address unmet needs. In particular, the emergence of FGFR inhibitors has highlighted the importance of genetic mutation diagnostics to quickly detect the presence of such mutations. (from the left) Professor Tae-Jung Kim, Professor Inho Kim, BU director Yeon-Hee Kim Inho Kim, professor of Oncology at Seoul St. Mary's Hospital, and Tae-Jung Kim, professor of pathology at Yeouido St. Mary's Hospital, emphasized the importance of diagnosing FGFR mutations at a press conference held by Janssen Korea on the 16th, which was held to celebrate the launch of Balversa. Balversa was approved by the Ministry of Food and Drug Safety in January 2022. However, it is still not reimbursed in Korea. Specifically, the drug is indicated for the treatment of adult patients with locally advanced or metastatic urothelial carcinoma (mUC) with FGFR2 or FGFR3 genetic alterations whose disease has progressed on or after at least one line of prior systemic therapy, which includes platinum-based chemotherapy, or whose disease has progressed within 12 months of neoadjuvant or adjuvant treatment with platinum-based chemotherapy. However, the approval of PD-1 and PD-L1-directed immuno-oncology agents in the first- and second-line settings that followed Balversa’s approval led to the need for Balversa to demonstrate efficacy in patients who previously received these agents. The situation was addressed with the publication of Balversa’s Phase III THOR trial study, which demonstrated a prolonged overall survival (OS) benefit with Balversa over chemotherapy in patients with metastatic urothelial carcinoma with FGFR3/2 gene alterations whose disease progressed after first-line treatment with immuno-oncology agents. In the study, Balversa prolonged overall survival (OS) compared with chemotherapy in patients with metastatic urothelial carcinoma. Results showed that over a median follow-up of 15.9 months, the mOS was 12.1 months in the Balversa arm, reducing the risk of death by 36% compared with the 7.8 months in the chemotherapy arm. Based on these findings, the U.S. Food and Drug Administration granted Balversa formal approval in January, but with a more restricted indication than originally approved. “Bladder cancer is most commonly diagnosed in those in their 60s and older, with frequent recurrences and metastases, so it is important to prevent metastases or treat recurrences and metastases early,” said Professor In-ho Kim. “There is a significant unmet therapeutic need, especially for patients with distant metastases, where the 5-year relative survival rate is only 11.7%.” ‘Balversa is the first targeted therapy for bladder cancer, which is significant because it improves survival in patients who have exhausted both chemotherapy and immuno-oncology options and provides an opportunity for further treatment,’ added Professor Kim. The second speaker, Professor Tae-Jung Kim, emphasized the importance of early diagnosis of FGFR mutations in bladder cancer patients. ‘FGFRs play a significant role in signaling pathways that regulate cell growth, differentiation, survival and migration,’ said Professor Kim. ’FGFR mutations are found in a variety of cancers, but they are particularly common in bladder cancer, where they are observed in approximately 20% of patients.’ ‘The use of mutation-specific targeted therapies may help stop cancer proliferation and progression or improve the effectiveness of other treatments,’ he added. ’The NCCN guidelines also consider or recommend molecular/genomic testing for genetic mutations in some patients, such as those with bladder cancer tumor invasion grade IIIB or higher.’ In other words, for patients with bladder cancer who are in the chemotherapy phase, the guidelines recommend testing for genetic mutations in the early stages of treatment strategy planning. “We are pleased to be able to offer a new treatment option in FGFR-mutated urothelial cancer with Balversa. We plan to communicate the clinical benefits and emphasize the importance of mutation diagnosis so that more patients can benefit from Balversa treatment.”

- Company

- 'Vorasidenib' receives Orphan Drug Designation in KOR

- by Eo, Yun-Ho Oct 18, 2024 05:49am

- 'Vorasidenib,' an anticancer drug targeting brain cancer, has been designated an orphan drug in South Korea. The Ministry of Food and Drug Safety (MFDS) announced this on October 8th through the Orphan Drug Designation (ODD) notice. Vorasidenib is an orally administered dual inhibitor of isocitrate dehydrogenase (IDH) 1/2 that selectively penetrates the blood-brain barrier. The drug's efficacy for selective malignant brain tumors (neuroglioma) was demonstrated through a double-blind Phase 3 clinical trial led by a research team at the University of California, Los Angeles (UCLA). The research team administered the targeted anticancer drug vorasidenib (40 mg single dose per day) or placebo to 331 patients with specified brain tumors (residual or recurrent Grade 2 glioma with IDH mutation) who have undergone brain tumor surgery as their only treatment. Grade 2 gliomas with isocitrate dehydrogenase (IDH) mutation are malignant brain tumors that cause considerable disability in patients, leading to early death. Gliomas tend to advance slowly but are fatal and affect people in their 30s. Study participants were randomly assigned to vorasidenib-treated patients (study group) and placebo-treated patients (control group). 168 of these patients took vorasidenib, and 163 took the placebo. Study results showed that the progression-free survival (PFS) for the vorasidenib-treated patient group was 27.7 months and that for the placebo-treated patient group was 11.1 months. Vorasidenib delayed the progression of malignant tumors by 16.6 months and lowered the death risk to 39%. Additionally, it improved the time until the next anticancer therapy (chemotherapy, radiotherapy), reducing the patient death risk to 26%. The side effects experienced by the vorasidenib-treated patient group were 22.8%, whereas 13.5% in the placebo-treated patient group. However, no significant side effects have been found. The primary endpoint was imaging based PFS and the secondary endpoint was the time to the next anticancer intervention. Of those study participants, 226 (about 68%) patients had a follow-up of 14.2 months (median value) and continued to take vorasidenib or placebo. At 30 months (Sept. 2022), 72% of the vorasidenib-treated patient group was still taking the drug and had not experienced disease progression. Meanwhile, France-based Servier Pharmaceuticals developed vorasidenib and is proceeding with the approval process in the U.S. and Europe.

- Company

- Will blockbuster contraception Mercilon find a new provider?

- by Nho, Byung Chul Oct 18, 2024 05:49am

- Product photo of Mercilon As Alvogen Korea and Chong Kun Dang's co-promotion contracts for oral birth control pills are set to expire, many pharmaceutical·distributors are sending love calls. Sources said that distributors, including pharmaceutical companies with strength in over-the-counter drug sales, have visited Alvogen Korea and Chong Kun Dang to weigh considerations. Alvogen and Chong Kun Dang signed a domestic distribution agreement for Mercilon in 2019. Alvogen has been responsible for the approval·imports·marketing of the drug, and Chong Kun Dang has been responsible for pharmacy sales. At the time, Alvogen chose Chong Kun Dang as the Korean partnership company for Mercilon because it had a variety of line-ups for female diseases and a nationwide pharmacy sales network. Chong Kung Dang has a variety of OTC products for women, including the painkiller PENZAL, Prefemin for premenstrual symptoms, the anemia treatment Bolgre, and the prenatal nutritional supplement Gowoonzymemom. As it is relates to the sales agreement, Alvogen and Chong Kun Dang are remaining silent about 'The termination due to contract maintenance·expiration.' There are opinions that, considering continued generation of sales, Chong Kun Dang may retain the sales rights. Based on pharmaceutical sales performance, Mercilon generated KRW 2.97 billion until the first half of the year, ranking no.1 in the product line containing desogestrel·ethinyl estradiol. Mercilon's exterior growth for 2020·2021·2022·2023 were KRW 7.6 billion·KRW6.9 billion·KRW6.9 billion·KRW7.2 billion. However, if a company proposes conditions like dramatic sales growth, considerable commission reduction, or even taking over all the remaining stock (estimated at KRW 6 billion), another company may acquire the sales rights because Alvogen has nothing to lose. Meanwhile, companies that are likely to get sales growth upon acquiring Mercilon sales right include Dongkook Pharmaceutical, Kwangdong Pharmaceutical, and ZP Therapeutics. Dongkook Pharmaceutical launched the third-generation birth control pill in 2020, but it has not caused a significant shift in the market. Kwangdong Pharmaceutical has Sunhana·Senselibe. However, they have generated KRW 28 million and KRW 1.1 billion, respectively. ZP Therapeutics acquired approval rights for Actinum in 2022, and the company has been actively pursuing sales and marketing. Considering this situation, these pharmaceutical companies are guaranteed annual sales of about KRW 10 billion when they acquire the sales rights of Mercilon, which is close to blockbuster. However, considering the co-promotion fee is 8-15%, the net gain may be lower than their in-house OTC sales. Meanwhile, Mercilon has ranked No.1 in OTC oral birth control pills. It shows contraceptive effects by combining the actions of ethinyl estradiol, estrogen, and desogestrel, progesterone. The clinical trials for Mercilon have been completed in 12 European countries. Mercilon is a global brand sold in 42 companies worldwide.

- Company

- oHCM drug Camzyos's last hurdle to reimb remains high

- by Eo, Yun-Ho Oct 15, 2024 05:50am

- The reimbursement journey for ‘Camzyos’, which is seeking insurance reimbursement in Korea, is going to be a rocky road until the end. According to industry sources, the drug pricing negotiations between BMS Pharmaceuticals Korea and the National Health Insurance Service (NHIS) for the obstructive hypertrophic cardiomyopathy (oHCM) drug Camzyos (mavacamten) have been extended after failing to finalize the deal within the deadline. The deadline extension was primarily due to a disagreement over the number of patients eligible for Camzyos. Camzyos’ reimbursement journey faced difficulties, receiving a redeliberation decision from the Health Insurance Review and Assessment Service's Drug Reimbursement Evaluation Committee. The drug passed the committee and entered pricing negotiations in August, but the negotiations were not concluded within the 60-day deadline. Camzyos is the first and only cardiac myosin inhibitor that specifically targets excess cross-bridge formation of myosin and actin proteins, the main cause of oHCM. It improves left ventricular hypertrophy and left ventricular outflow tract obstruction by separating myosin from actin, relaxing the overcontracted heart muscle. Due to the lack of a cure, oHC has long been managed with off-label drug use. In fact, the European Society of Cardiology (ESC) revised its HCM guidelines for the first time in 9 years with the introduction of Camzyos. Before then, HCM guidelines have been based on small observational data reported from individual institutions, retrospective analyses, or expert consensus opinions. Therefore, Camzyos was a game-changer in the field. After demonstrating its significant effect in two large-scale Phase III randomized controlled trials (RCTs), Camzyos was recommended at the highest evidence level, A, for the first time among treatment options in the ESC guidelines. The American College of Cardiology (ACC) and American Heart Association (AHA) are also currently preparing to update their guidelines. Based on the Phase III trial data, Camzyos received a breakthrough therapy designation (BTD) and was approved by the US FDA. In the Phase III EXPLORER-HCM trial, which served as the basis for Camzyos’s approval, Camzyos achieved and improved the primary composite endpoint of the proportion of patients with decreased symptom burden (by NYHA class) and functional capacity (peak oxygen consumption, pVO2) by more than 2 times compared with placebo. In particular, 20% of the patients who received treatment with Camzyos achieved both primary endpoints, pVO2 improvement, and the NYHA class requirement. Also, the dynamic left ventricular outflow tract obstruction was reduced by over 4 times with the use of Camzyos. 7 out of 10 patients treated with Camzyos improved to the extent that they would not consider surgery, and showed consistent benefits over 30 weeks. “Many patients with oHCM have been anxiously awaiting a new drug due to the lack of a suitable treatment,” said Hyung-Kwan Kim, Professor of Cardiology at Seoul National University Hospital. “In particular, expectations for the drug's reimbursement have increased since it was approved by DREC in July, and we hope that the remaining procedures will be completed as soon as possible so that patients and their caregivers in Korea can benefit from the use of the new drug.”

- Company

- “Market for veterinary drugs expected to grow rapidly”

- by Son, Hyung Min Oct 15, 2024 05:50am

- Seung-Hwan (SH) Jung, General Manager at MSD Animal Health Korea “MSD Animal Health Korea’s clients are animals. We believe that the drug distribution channels for animals should be carefully designed to contribute to the health of animals in Korea. Supplying our products to animals that need them quickly, sufficiently, and safely is the biggest principle in designing our domestic distribution network. Seung-Hwan (SH) Jung, General Manager at MSD Animal Health Korea, emphasized so to reporters about the company’s plans for supplying veterinary drugs in Korea. Over the years, MSD Animal Health Korea has launched various new products and provided technical support to meet the needs on-site. In doing so, the company has prevented and treated diseases in economic and farm animals and contributed to improving the productivity of farmers and the health and welfare of companion animals in Korea. MSD Animal Health Korea's flagship products include the ‘Porcilis PVC M Vaccine,’ which prevents the Porcine Circo Virus (PCV) and M.hyo, and the ‘Prime Pac PRRS Vaccine,’ which prevents Porcine Reproductive and Respiratory Syndrome in the swine industry; ‘Exzolt,’ a parasiticide for chickens that eliminates mites; ‘Nobilis SG9R Vaccine,’ which prevents chicken typhoid. The company also has ‘Bravecto,’ which prevents ectoparasites in pets, and ‘Caninsulin,’ the only insulin for pets in Korea. “The global veterinary drug market is estimated to be around USD 45.8 billion in 2023, of which our sales recorded USD 5.6 billion,’ said Jung. “The animal health sector is generally divided into ruminants, poultry, swine, aquaculture, and companion animals, and MSD Animal Health is the global sales leader in four of these five categories, except for companion animals.” In Korea, the veterinary drug market is estimated to be worth around KRW 1.4 trillion, with two-thirds of the market being domestically produced and one-third being imported. MSD Animal Health Korea generated sales of KRW 45 billion last year. ‘Our main business areas in Korea are swine, poultry, and companion animals,’ says Jung. In terms of total sales, the swine and poultry division accounts for the largest share, but we are also expecting rapid growth in the companion animal and livestock sectors.” “Due to issues such as superbugs, most developed countries, including Korea, have banned the addition of growth-promoting antibiotics to feed, and it is becoming increasingly difficult to use therapeutic antibiotics in livestock,’ he explained. ’Personally, I see this as a positive change that is in line with the concept of One Health, which has a common goal of seeking animal and human health. As a result, I believe the veterinary drug industry is also shifting towards prevention rather than treatment, promoting the use of vaccines rather than antibiotics.’ Jung also sees much growth potential in the domestic animal health market. With the rise in the number of people living with companion animals, the demand for animal healthcare has been growing along with the market. “The sector has been growing at an average annual growth rate of 10% with the rising demand for pet healthcare,” said Jung. “The scale of the swine and poultry industry is also large compared to Korea’s population. In particular, consumer demand is shifting to seeking safe animal products from the abundance of animal products in the past. We believe that the use of veterinary drugs to prevent diseases and promote animal welfare in farm animals, including food poisoning and zoonotic diseases, will continue to increase.” Various channels such as veterinary hospitals and pharmacies...”We plan to distribute ETCs and OTCs separately” MSD Animal Health Korea plans to utilize various distribution channels such as veterinary clinics and pharmacies. The veterinary drug market is being developed similarly to that of human drugs such as digestive and diabetes diseases, using various channels. And many pharmaceutical companies, including MSD Animal Health Korea, are looking to enter the field. “The specialization of veterinary drugs is predictable in the same way as the changes we have seen in human medicines,” said Jung, “and we interpret this as a favorable change for our business because we own many products that are unique to MSD Animal Health that other companies do not have.” ‘MSD Animal Health employees around the world are sensitive to changes in the market and disease outbreaks, and these changes are immediately reported to R&D at headquarters, resulting in new products being developed to respond quickly to changes in the market as well as diseases. We expect this strength to persist.’ MSD Animal Health's mission is ‘The science of healthier animals’. At the end of the day, Jung says, MSD's customers are animals, and providing products for healthy animals is the company's number one goal. “We are considering carefully designing the distribution channels of our medicines to contribute to animal health,” said Jung. “The overarching principle of our distribution network design is to get our products to the animals that need them quickly, sufficiently, and safely.” ‘We plan to establish different distribution networks for specialized and over-the-counter products. We will design a new distribution network in the future based on domestic laws.’